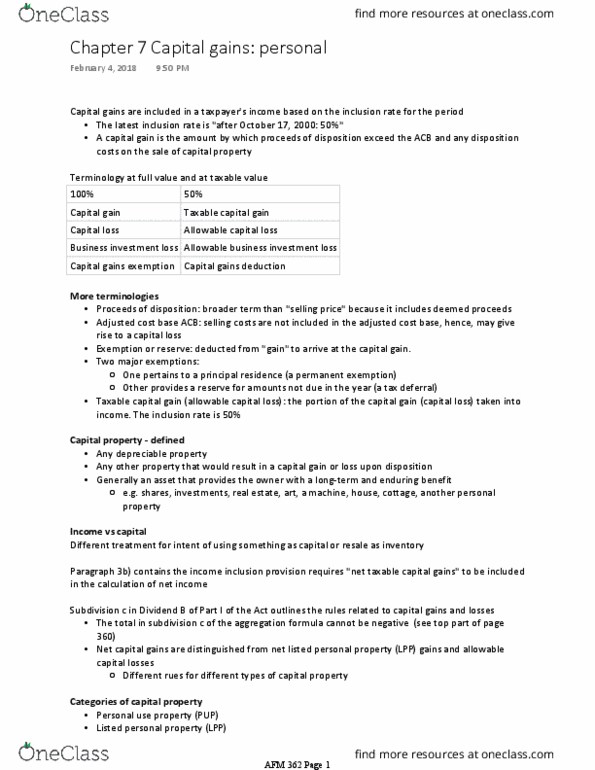

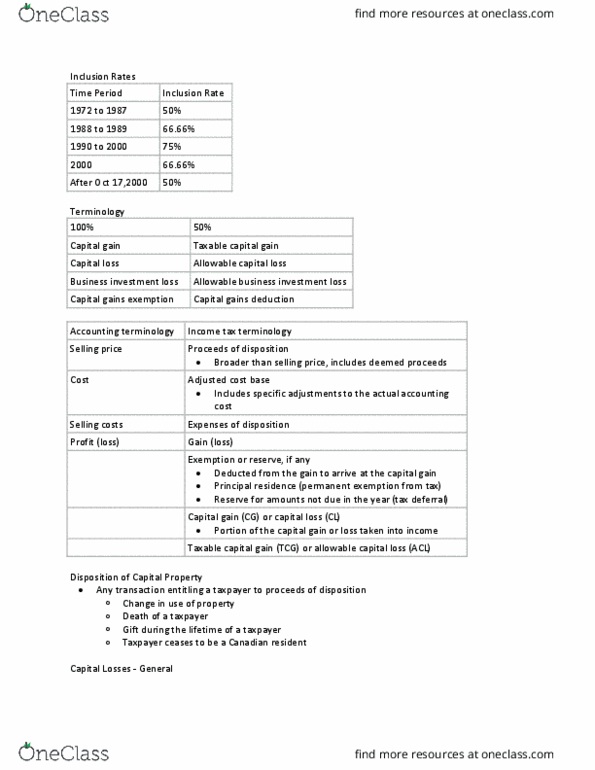

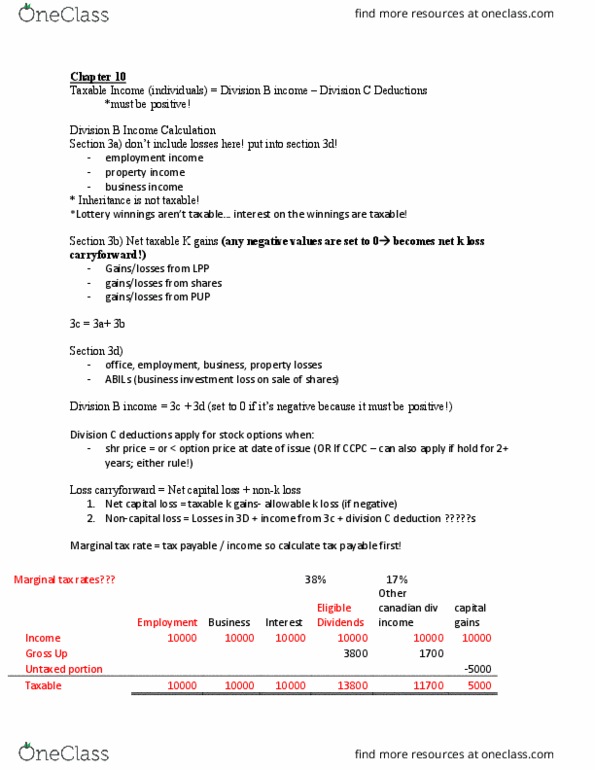

AFM362 Lecture Notes - Lecture 20: Capital Loss, Property Income, Investment

Document Summary

Get access

Related Documents

Related Questions

1.Which of the following statements about conversion of income is correct?

| a. | converting ordinary income into capital gain is a beneficial tax planning strategy | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| b. | converting capital gain income into ordinary income is a beneficial tax planning strategy | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| c. | converting qualifying dividends into interest income is a beneficial tax planning strategy | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| d. | holding assets that will generate a capital gain inside a retirement plan is a beneficial tax planning strategy 2. Which of the following statements is NOT a true statement regarding long-term capital assets?

|

During the current year, Marlene, Nancy and Olive formed a new SCorporation. Solely in exchange for stock, Marlene and Nancycontributed appreciated property, while Olive contributed services.The exchanges of Marlene and Nancy will be nontaxable if:

Olive receives 30% of the stock | ||

Olive receives 80% of the stock | ||

Olive receives 15% of the stock | ||

Marlene and Nancy together receive 50% of the stock |

In June of 2018, Alice acquired heronly machine for $30,000 to use in her business. The machine isclassified as 5-year property. Aliceâs maximum depreciation(including bonus) on the machine this year is:

$30,000 | ||

$12,000 | ||

$6,000 | ||

$18,000 |

Cactus Corporation, an S Corporation, had accumulated earningsand profits of $200,000 at the beginning of the tax year. Tex andShirley each own 50% of the stock. During the current year Cactushad $100,000 of ordinary income and distributed $10,000 to Tex and$10,000 to Shirley. What is Tex's taxable income for the currentyear?

$10,000 | ||

$0 | ||

$100,000 | ||

$50,000 |

Bristol Corporation was formed as an S Corporation on January 1,2014 and elected S corporation status at that date. Bristol has hadthe same 25 shareholders throughout its existence and has one classof stock. Bristol's S election will terminate if it:

10% of the shareholders vote to revoke the election | ||

to purchase 10 shares | ||

Allows a variation in the voting rights of the stock | ||

Increases the number of shareholders to 125 |

On February 10, 2018, Ace Corporation, a new calendar yearcorporation, elected S corporation status and all shareholdersconsented to the election. There was no change in its shareholdersduring the current year. Ace met all eligibility requirements foran S corporation during the preelection portion of the year. Whatis the earliest date on which Ace can be recognized as an Scorporation?

February 10, 2018 | ||

January 1, 2019 | ||

February 10, 2019 | ||

January 1, 2018 |

In March of 2017 Frederick acquired an passenger automobile for$45,000 and used the automobile 85% for business. Themaximum depreciation deduction for 2017 is:

$3,160 | ||

$11,160 | ||

$8,928 | ||

$9,486 |

In August of 2017, Joseph acquires andplaces into services business equipment costing $300,000. Theequipment is classified as 5-year recovery property. No otheracquisitions are made during the year. Joseph elects to expense themaximum amount under Sec. 179. Josephâs total deductions for theyear are

$60,000 | ||

$500,000 | ||

$100,000 | ||

$300,000 |

For the current tax year, VBN, an S Corporation distributes$100,000 to its sole shareholder, Raymond. His basis in the stockwas $140,000 before the distribution. VBN had once been a regular CCorporation and had remaining accumulated earnings and profits(E&P) from those years of $70,000. However, VBN has no balancein its accumulated adjustment account. How should the distributionof $100,000 be handled?

$100,000 as a taxable distribution

$70,000 as a taxable dividend, and $30,000 has a non taxablereturn of capital

$50,000 as a taxable dividend, and $100,000 as a non taxablereturn of capital

$70,000 as a taxable dividend; and $30,000 as a capital gain

Stahl, an individual who owns 100% of Talon, an S corporation,had a basis of $50,000 at the first of the year. During the yearTalon reported the following: Ordinary Loss of $10,000; Municipalinterest income of $8,000, Long term capital gain of $4,000; andLong term capital loss of $9,000. What was Stahl's basis in Talonat year end?

$56,000 | ||

$65,000 | ||

$53,000 | ||

$43,000 |

Gross Receipts of $70,000; Tax Exempt Interest Income of $4,000;Dividends of $10,000; Supplies Expense of $3,000; and UtilitiesExpense of $1,500. What amount is the S Corporation's ordinarytaxable income?

$75,500 | ||

$79,500 | ||

$70,000 | ||

$65,500 |

Bob and Sam each owned 50% of Lostalot, an S Corporation. Bob'sbasis is $30,000 and Sam's basis is $15,000. The corporation hasoperating loss for the current year of $50,000. Howmuch loss can each shareholder deduct in the current year assumingthey materially participate in the business:

Bob: $25,000; Sam: $15,000 | ||

Bob: $0; Sam: $0 | ||

Bob: $25,000; Sam: $25,000 | ||

Bob: $30,000; Sam: $15,000 |

Terra Corporation, a calendar-yeartaxpayer, purchases and places into service in 2017 machinery witha 7-year life that cost $650,000. The mid-quarter convention doesnot apply. Terraâs taxable income for the year before the Sec. 179deduction is $700,000. What is Terraâs total maximum depreciationdeduction related to this property?

$585,718 | ||

$521,345 | ||

$92,885 | ||

$500,000 |

Identify which of the following statements is false.

The PTI (previously taxed income) represents the balance ofundistributed net income which were already taxed. | ||

The AAA balance can be negative, but the shareholder's basis inthe S corporation stock cannot be less than zero. | ||

Tax exempt income increase the AAA and the basis of the Scorporation stock. | ||

| An S Corporation may or may not have accumulated Earnings andProfits Elaine owns an unincorporated manufacturing business. In 2017,she purchases and places in service $600,000 of qualifying fiveyear equipment for use in her business. Her taxable income from thebusiness before any section 179 deduction is $100,000. Which of thefollowing statements is true? |

Elaine cannot deduct any Section 179 deduction for 2017 | ||||||||||||||

Elaine can deduct $100,000 as a Section 179 deduction in 2017with a $400,000 carryover to next year. | ||||||||||||||

Elaine can deduct $100,000 as a Section 179 deduction in 2017with a $500,000 carryover to the next year | ||||||||||||||

| Elaine can deduct $500,000 as a section 179 deduction in2017 Charles, an individual, owned 100% of the Alpha, an Scorporation. At the first of the year, Charles' basis in Alpha was$25,000. In the current year, Alpha realized ordinary income of$1,000; and a long term capital gain of $3,000. Alpha distributed$25,000 to Charles at the end of the year. What amount of the$25,000 is taxable to Charles?

|