AFM362 Lecture Notes - Lecture 10: Term Life Insurance, Employee Benefits, Life Insurance

22 Apr 2017

School

Department

Course

Professor

Document Summary

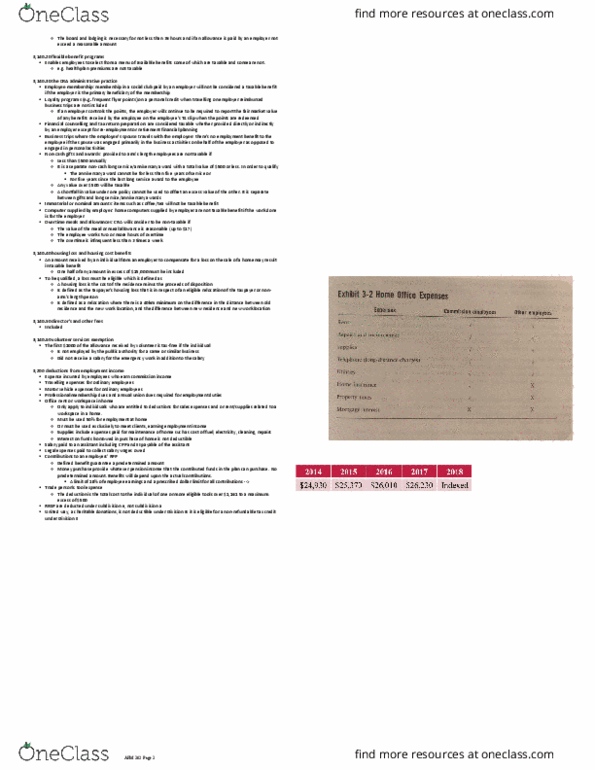

Chapter 3: employment income is reported on a calendar-year basis, tax year for individual ends. December 31 remuneration = direct benefits + indirect benefits. Stock options: employment income: fv shrs when option exercised option price paid for shares capital gain/loss: proceeds of disposition on sale of shares fv shrs when options are exercised. If applicable, of employment income from stocks. Automobile benefits = standby charge + operating benefit: standby charge: benefit employee receives from having use of a capital asset, employer owned vehicles = a/b *[ 2%* (c*d), employer leased vehicles =a/b * [2/3 (e-f)] A= lesser of personal use km or b (if more personal use, a=b therefore a/b=1) B= 1667 * (total days available/30), total days available = 365 if for full year. C = full original cost of car + hst. F= portion of lease payments related to insurance operating benefit: the benefit received from not paying for operating cost of car.