BADM*1060 Lecture Notes - Lecture 4: Current Liability, Cash Flow Statement, Book Value

Document Summary

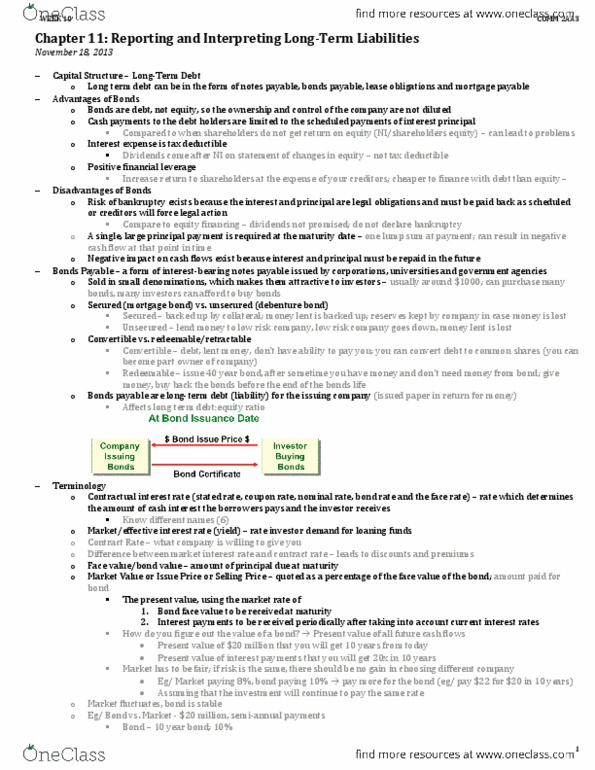

Obligations to be paid after one year. Normally repayable in a series of periodic payments called instruments. May be secured by specific assets which are commonly referred to as mortgages. Installment payments usually take one of two forms: fixed principle payments plus interest (fixed or floating interest, blended principal and interest payments. A form of interest-bearing notes payable issued by corporations, universities, and government agencies. Sold in small denominations, which makes them attractive to investors. Stated rate which determines the amount of cash interest the borrower pays and the investor receives. Bond face value to be received at maturity, and: 2. Interest payments to be received periodically after considering current interest rates. The effective-interest method is used to amortize bond discount or premium. With the effective-interest method the interest expense reflects the same percentage of the (cid:271)o(cid:374)d"s (cid:272)a(cid:396)(cid:396)(cid:455)i(cid:374)g a(cid:373)ou(cid:374)t ea(cid:272)h pe(cid:396)iod. Amortization spreads the cost of borrowing over the life of the bond.