ADM 3349 Lecture Notes - Lecture 4: Financial Statement, General Ledger, Limited Liability Partnership

12 Apr 2016

School

Department

Course

Professor

Document Summary

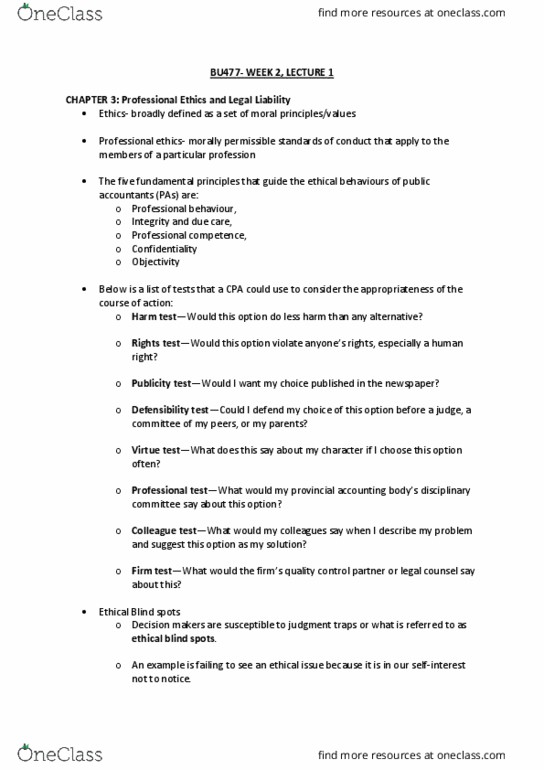

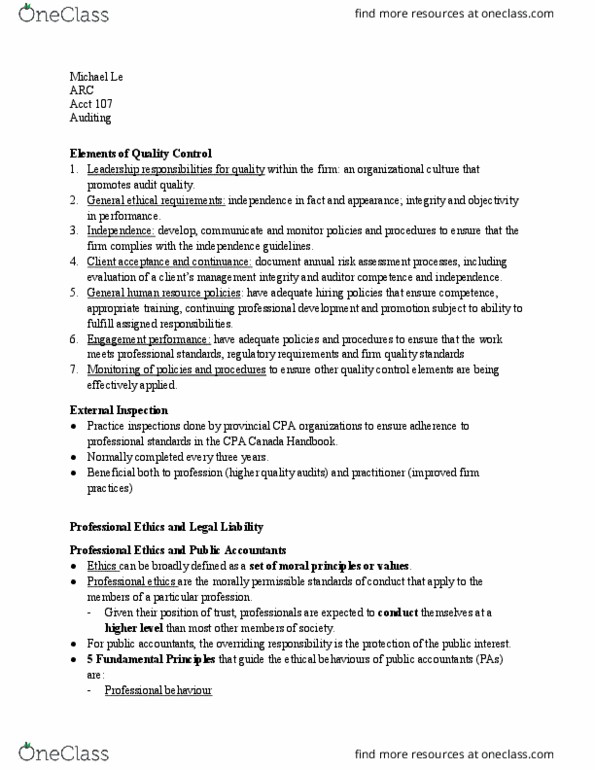

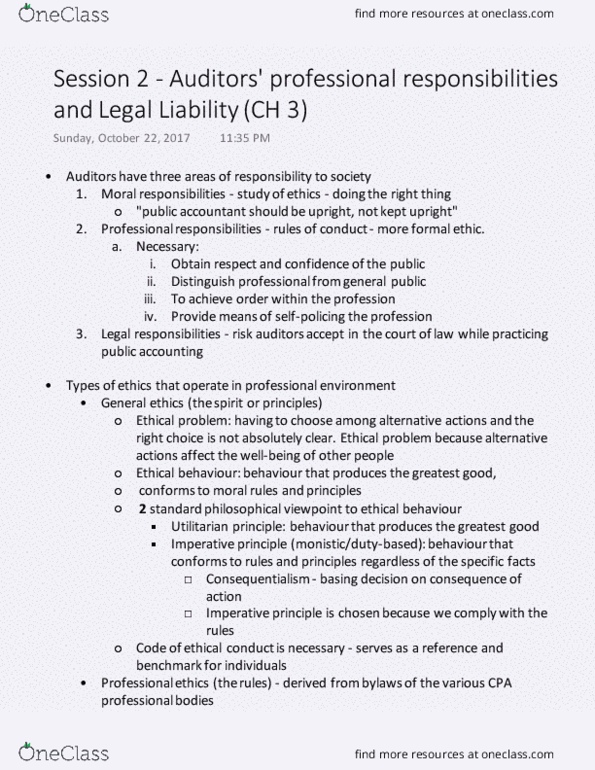

Chapter 3 - auditor"s ethical and legal responsibilities. Ethics - broadly deined as a set moral principles or values that one chooses, and is also concerned with the consequences of decisions. Serves both the members of the body promulgaing the code and the public. Public accountants, provincial insitutes and the order have harmonized rules of professional conduct. Profession moving to apply rules to public accouning irms, and students. Cica/cgaac/smac codes of conduct aim for general statements of ideal conduct, and speciic rules. Common principles; public interest, integrity and due care, conideniality, reputaion, professionalism, independent or objecive state of mind. Generally required for all types of assentaion engagements, in accouning and audiing we must be individual (and separate) of the businesses that we work for. Independence in fact: the idea that one is actually is independent of the client. Independence in appearance: appearing to be independent to the business or client that you are working for.