MGEC61H3 Lecture Notes - Interest Rate Parity, Foreign Exchange Spot, Foreign Exchange Market

29 Nov 2013

School

Department

Course

Professor

Document Summary

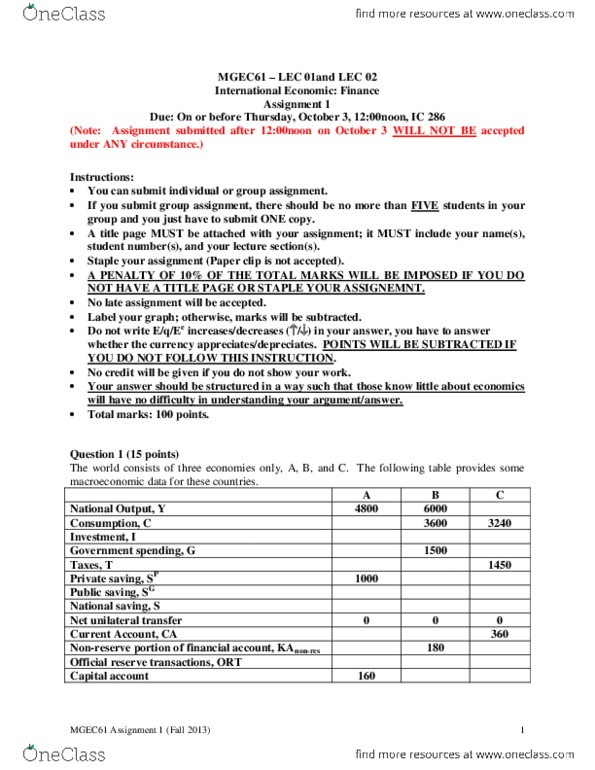

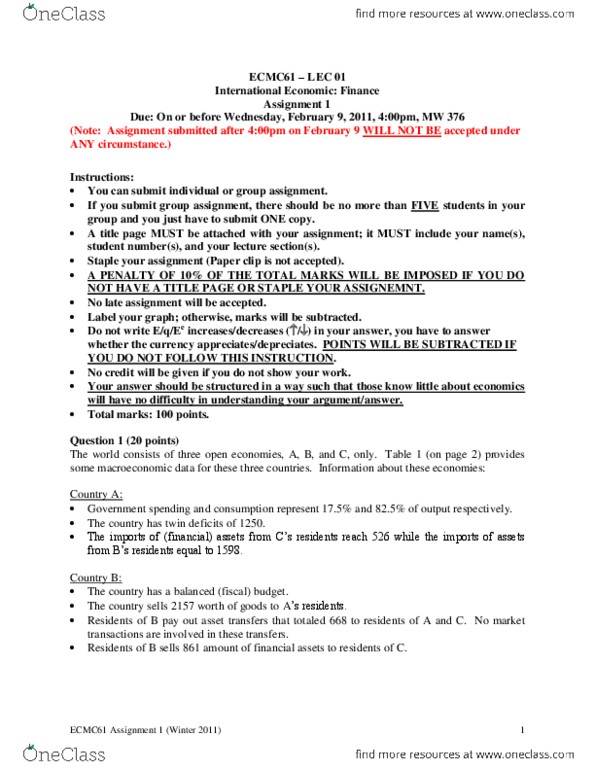

Bop = ca + kanon-res + capital account. Country c. 360 380 + 210 = 190. Answer for question 1 part a (submit this page with your answers in your assignment for grading) Assume the domestic currency has a higher nominal interest rate than the foreign currency, then the investors will invest in domestic currency deposits, this will cause net capital inflows, which creates upward pressure for the domestic currency to. Appreciate, that push back exchange back to the point where interest rate parity holds, where the return on the dc = the return on the fc. Given by question: spot exchange market e /a$ = 100. 6, given by question that australian dollar is traded at a forward premium of 1. 1% against the. Japanese yen, in other word we can also understand that japanese yen is traded at a forward discount of 1. 1% against australian dollar.