MGAB02H3 Lecture Notes - Lecture 1: Debits And Credits

24 Mar 2015

School

Department

Course

Professor

Document Summary

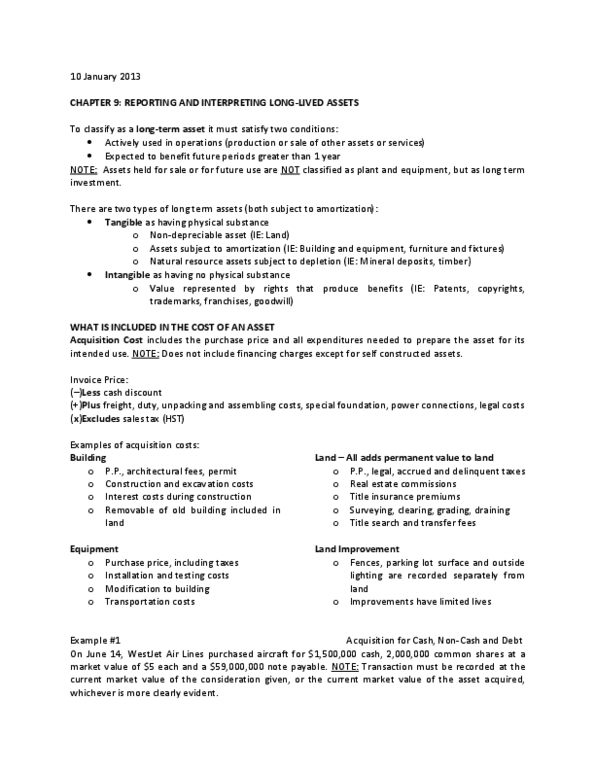

Purchase a building and pay $ 600,000 in cash. Purchase a building and pay $ 300,000 in cash and the rest is financed through a bank loan. The value of the building = $ 600,000. Purchase a building for $ 600,000 = paid $ 300,000 in cash and the rest is through the issuance of common shares. Purchase the building for $ 600,000 and th eowner of the builidng is giving a term of 2/10, net 30 for the customer to pay. Assume the company paid within the discount period. Assume the company did not pay within the discount period. 600,000 ($ 600,000 x 2%) basket purchase - purchase different assets in bulk. Paid $ 2,000,000 to purchase land, building and equipment. Needs to break down th evalue by each asset. Use fv from each asset individually to allocate the purchase price. Ifrs requires the assets be recorded based on componentization.