MGAB02H3 Lecture Notes - Lecture 4: Interest Expense, Financial Statement, Cash Flow

6 Jan 2016

School

Department

Course

Professor

Document Summary

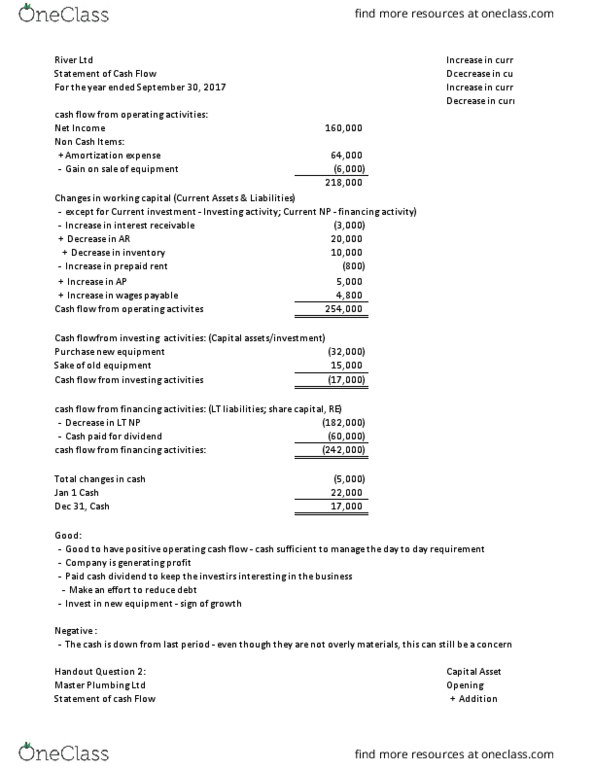

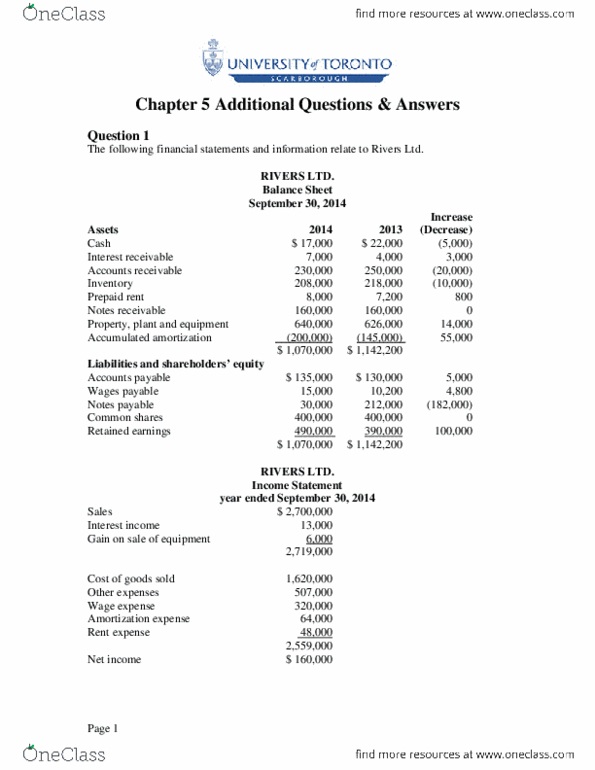

Increase in trade receivables (,000 ,000) (5,000) Decrease in inventory (,000 ,000) (3,000) Decrease in trade payables (,000 ,000) Decrease in wages payable (,000 ) (200) Increase in income tax payable (,000 ,000) During 2014, the company also purchased machinery for ,000, which was partially financed with a four-year ,000 note payable to the dealer. **income taxes paid = income tax expense increase in income taxes payable. The quality of earnings ratio measures the portion of income that was generated in cash. The ratio is greater than 1 primarily because of the large non-cash depreciation expense that reduced net earnings but did not affect cash. Cash flow from operations = ,000 = 1. 26. The capital expenditures ratio measures the company"s ability to finance plant and equipment purchases from operations without the need to issue shares, borrow from creditors, or to sell long-lived assets.