MGAB03H3 Lecture Notes - Lecture 6: Icq, Income Statement, Finished Good

8 Oct 2015

School

Department

Course

Professor

Document Summary

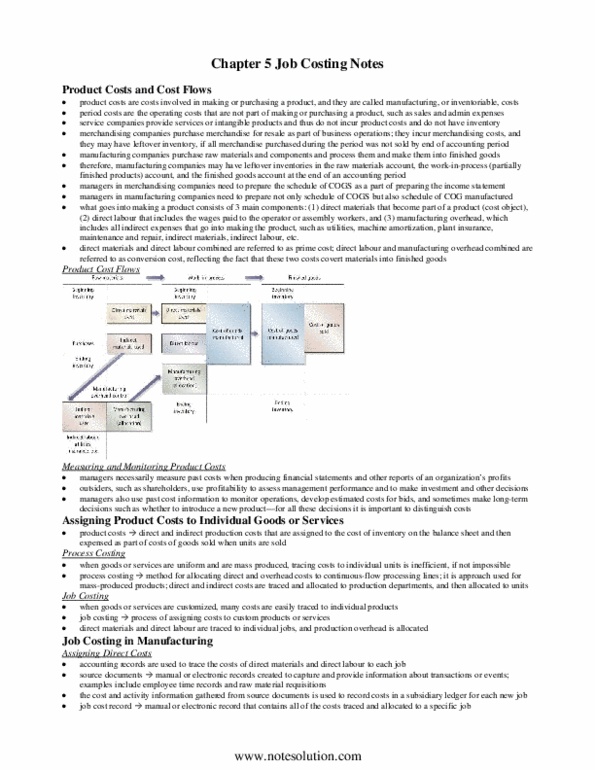

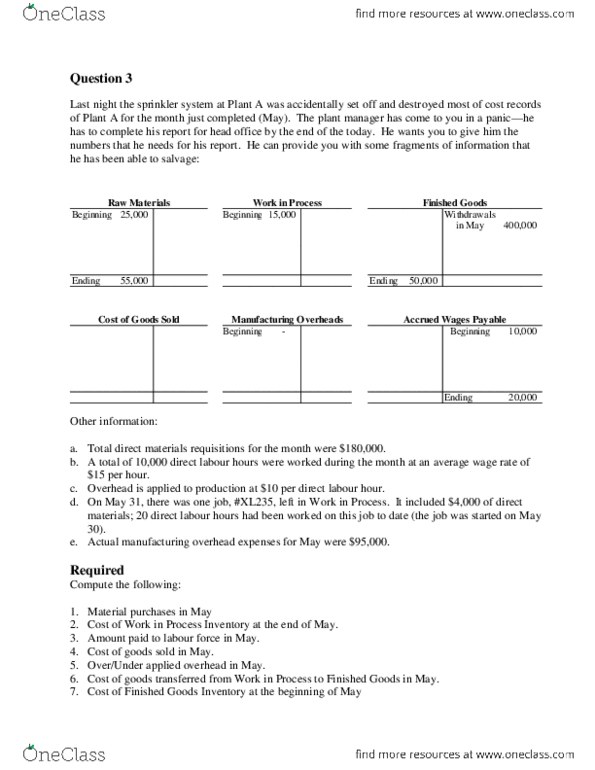

5. 21 schedule of cost of goods manufactured, cost of goods sold, income statement . 277,000: prime costs = direct materials + direct labour = 95,200 + 88,200 = 183,400. Conversion costs = direct labour + manufacturing overhead = 88,200 + 104,000 = 192,200. Job costing, over- and underapplied overhead, journal entries - shane"s shovels: notice that the company uses normal costing (overhead is allocated using an estimated rate). However, under normal costing the company is required to make an end-of-period adjustment for any overapplied or underapplied overhead. This means that the after- adjustment costs assigned to jobs completed will be actual cost: ,000: this month overhead was underapplied by ,000. This is the difference between total overhead costs of ,000 (indirect materials of ,000 plus other manufacturing overhead incurred of ,000) and manufacturing overhead allocated of ,000: work in process. The problem states that beginning and ending wip inventories were both zero.