MGAD65H3 Lecture Notes - Lecture 16: Max Boot, Capital Loss

14 Oct 2017

School

Department

Course

Professor

Document Summary

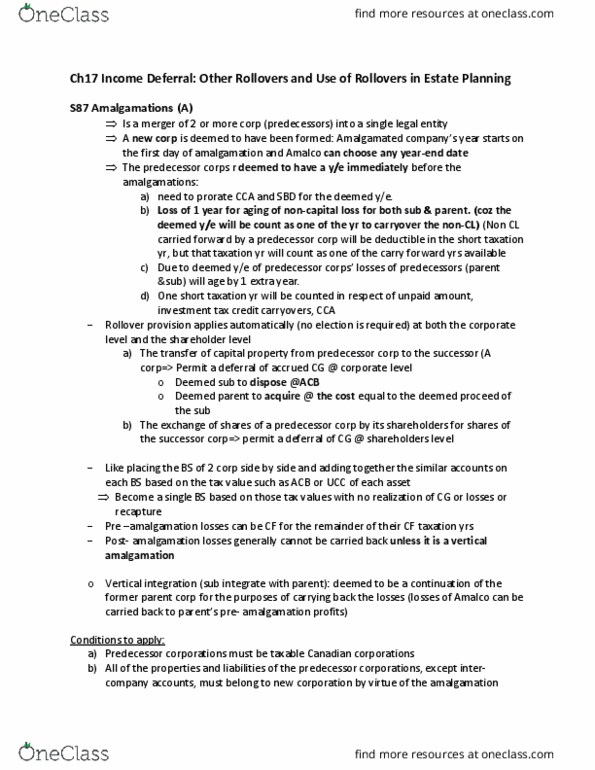

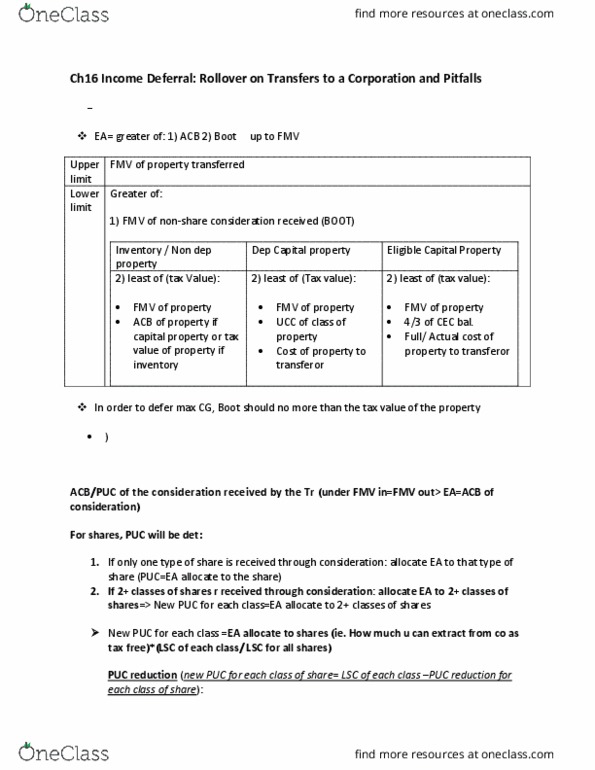

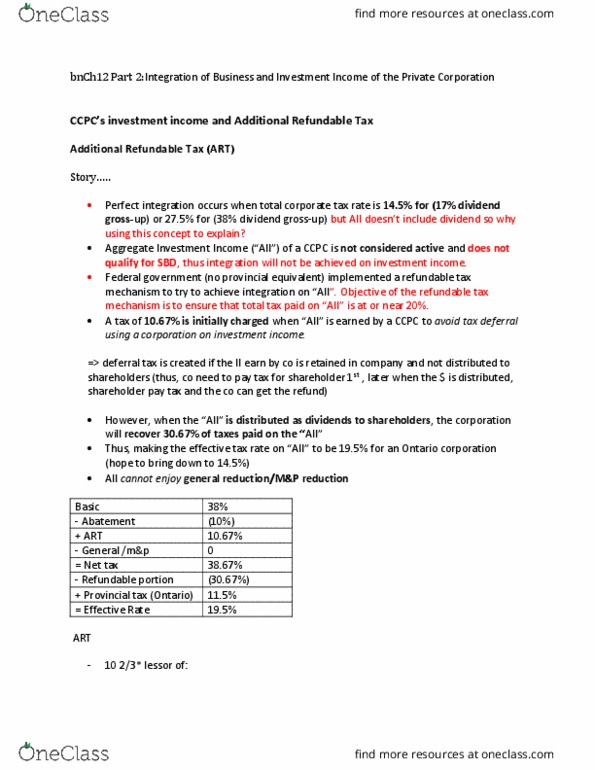

S85(1: (1) transfer of property to corporation by shareholders where a taxpayer has, in a taxation year, disposed of any of the taxpayer"s property that was eligible property to a taxable. Canadian corporation for consideration that includes shares of the capital stock of the corporation, if the taxpayer and the corporation have jointly elected in prescribed form and in accordance with subsection (6), the following rules apply: For consideration that includes shares: joint election (without s85 (1), if want to transfer asset to corp-> asset deemed to be disposal @ fmv-> thus, trigger cg (this is unrealized tcg-> not fair to pay tax)) Under s85(1), the income (ex cg, recapture) deferred @ the time of rollover will be t(cid:396)igge(cid:396)ed if the sha(cid:396)es (cid:396) sold i(cid:374) a(cid:374) a(cid:396)(cid:373)"s le(cid:374)gth t(cid:396)a(cid:374)sa(cid:272)tio(cid:374)=> defer income. S85 need not to be used when there is no accrued income to defer.