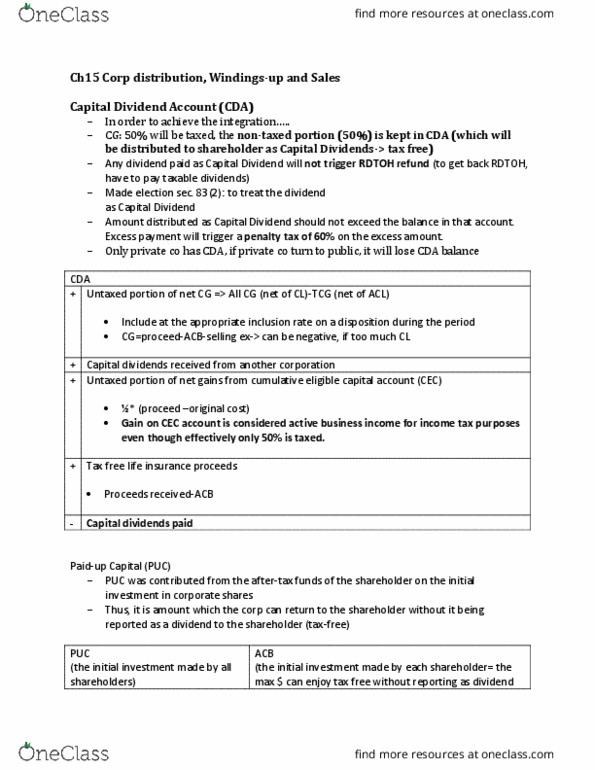

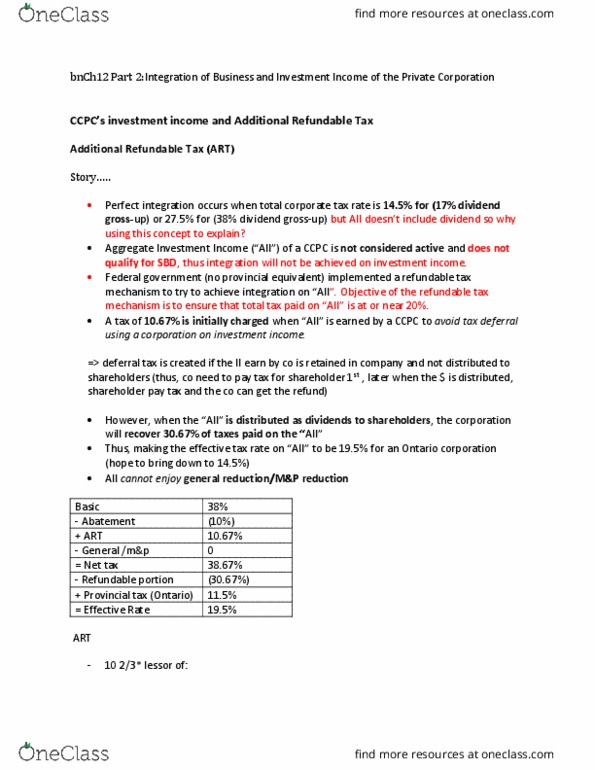

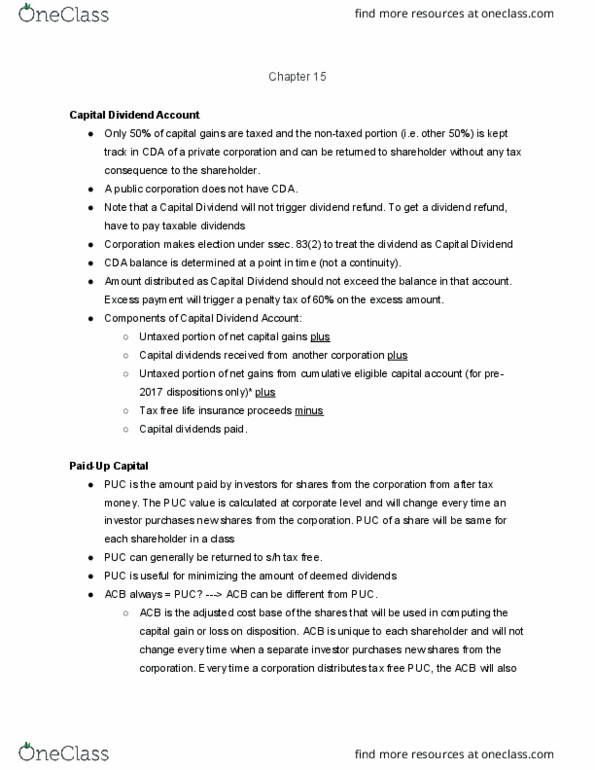

MGAD65H3 Lecture Notes - Lecture 13: Fide, Dividend, Accrual

67 views5 pages

14 Oct 2017

School

Department

Course

Professor

Document Summary

Ch13 planning the use of a corporation and shareholder- manager. The shareholder of the ccpc is usually the president, ceo, or director of that corporation. > choose the compensation package( salary vs dividend) to min the income tax. Dividend: lower personal tax but pay from co after tax income, recovery of rdtoh. Sala(cid:396)(cid:455) : (cid:396)edu(cid:272)e (cid:272)o"s i(cid:374)(cid:272)o(cid:373)e, i(cid:374)(cid:272)lude i(cid:374) rrsp (must pay a reasonable amount of salary according to the value of the service his/her provided)=> if the co income above sbd limit, a reasonable bonus can reduce income. Accrued employee remuneration (such as salaries, wages, and retiring allowances, bonus and pension benefits) that are not paid before the year-end of the corporation must be paid within 179 days after the year-end to be deductible. If the corp. does not pay within 179 days of the year-end, then the accrued employee remuneration is deductible in the year it is paid instead of the year it is accrued.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

Selected transactions of Shadrach Computer Corporation duringNovember and December of 2016 are as follows:

| Nov. | 1 | Borrowed money from the bank byissuing a non-interest-bearing, $58,000, 90-day note. The note isdiscounted on a 12% basis. |

| 9 | Sold 125 computers with a 1-yearassurance-type warranty for $5,600 each on credit (ignore cost ofgoods sold). Past experience indicates that warranty costs average$110 per computer. | |

| 12 | Sold 125 software packages at $270each on credit (ignore cost of goods sold). With each softwarepackage, Shadrach offered a premium in the form of a USB drive forthe return of one proof of purchase. The offer expires June 30,2017. The cost of each USB drive is $5, and Shadrach estimates that80% of the premiums will be redeemed; therefore, 100 USB driveswere purchased on credit. | |

| 20 | Paid $2,000 in fulfillment of thewarranty agreement on several of the computers sold on November9. | |

| 30 | Accrued monthly vacation pay.Shadrach has 80 employees who are each paid an average of $180 perday. Shadrach has a policy of allowing each employee 12 daysâ paidvacation per year; the related liability is recorded on a monthlybasis. Employees are paid monthly. | |

| 30 | Paid monthly payroll. Grosssalaries were $430,000. No vacations were taken during November.Income tax withholdings of 20% are applicable to the salaries ofall employees. A F.I.C.A. tax of 8% for both employees andemployers is also applicable. These rates apply to all salariesbecause no employeeâs salary has exceeded the maximum wage limit.The state allows the corporation a 1% unemployment compensationmerit-rating reduction from the normal rate of 5.4%. The federalunemployment rate is 0.6%. Prior to October, each individualemployee had accumulated a gross salary in excess of $7,000 for2016. | |

| Dec. | 14 | Twenty proofs of purchase werereturned from the November 12 sale. |

| 29 | An individual filed suit againstShadrach for damages caused in a November 5 accident that resultedwhen a member of the sales force hit the individualâs car while onpersonal business. The amount of the suit filed was $1,450. Becausethe employee was on personal business, the companyâs insurancecompany will not pay the claim. In Shadrachâs attorneyâs opinion,the amount of the suit is reasonable; furthermore, the companybelieves it is likely to lose the suit. | |

| 31 | Accrued monthly vacation pay. | |

| 31 | Paid monthly payroll. Grosssalaries were $433,000. The salaries included $6,500 of vacationpay in the sales force and $3,300 of vacation pay in the officestaff. The F.I.C.A. tax rate still applies to all wages because noemployeeâs salary exceeded the maximum wage limit. | |

| 31 | Recorded presidentâs bonus. Thepresident receives a 10% bonus on any income over $240,000, beforededucting income taxes and the bonus. Shadrachâs effective incometax rate is 30%, and income before income taxes and bonus for 2016was $560,000. The bonus will be paid in January 2017. |

| Required: | |

| Prepare journal entries torecord the preceding transactions of Shadrach Computer Corporationfor 2016. Include year-end accruals. Round all calculations to thenearest dollar. |

Chart of Accounts

| CHARTOF ACCOUNTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shadrach Computer Corporation | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General Ledger | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

22) Boxer Corporation buysequipment in January of the current year with a 7-year class lifefor $15,000. The corporation expensed the $15,000 under Sec. 179.The deduction in the year of purchase for E&P purposes due tothe acquisition and expensing of the equipment is

| ||||||||||||||||||||||||

23) Maxwell Corporation reportsthe following results:

Maxwell's dividends-received deduction is

| ||||||||||||||||||||||||

24) Identify which of thefollowing statements is false.

| ||||||||||||||||||||||||

25) Exit Corporation hasaccumulated E&P of $24,000 at the beginning of the current taxyear. Current E&P is $20,000. During the year the corporationmakes the following distributions to its sole shareholder who has a$22,000 basis for her stock.

The treatment of the $15,000 August 1 distribution would be

| ||||||||||||||||||||||||

26) Current E&P does notinclude

| ||||||||||||||||||||||||

27) Identify which of thefollowing statements is true.

| ||||||||||||||||||||||||

28) Crossroads Corporationdistributes $60,000 to its sole shareholder Harley. Crossroads hasearnings and profits of $55,000 and Harley's basis in her stock is$20,000. After the distribution, Harley's basis is

| ||||||||||||||||||||||||

29) Hogg Corporation distributes$30,000 to its sole shareholder, Ima. At the time of thedistribution, Hoggs' E&P is $14,000 and Ima's basis in herstock is $10,000. Ima's gain from this transaction is

| ||||||||||||||||||||||||

30) One consequence of aproperty distribution by a corporation to a shareholder is

| ||||||||||||||||||||||||

31) Identify which of thefollowing statements is true.

| ||||||||||||||||||||||||

32) Which of the following isnot a reason for a stock redemption?

| ||||||||||||||||||||||||

33) Elijah owns 20% of ParkCorporation's single class of stock. Elijah's basis in the stock is$8,000. Park's E&P is $28,000. If Park redeems all of Elijah'sstock for $48,000, Elijah must report dividend income of

|