MGEA06H3 Lecture Notes - Reserve Requirement, Demand Deposit, Siemens S200

30 Nov 2010

School

Department

Course

Professor

2

MGEA06H3 Full Course Notes

Verified Note

2 documents

Document Summary

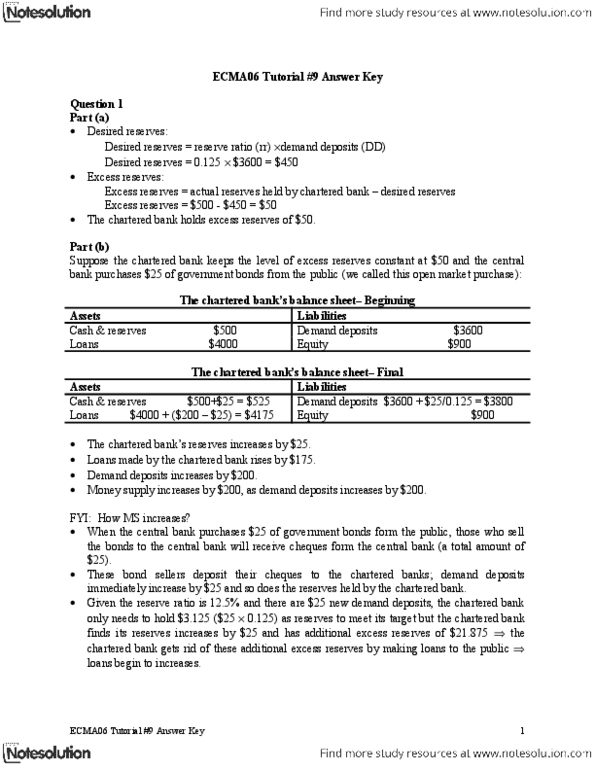

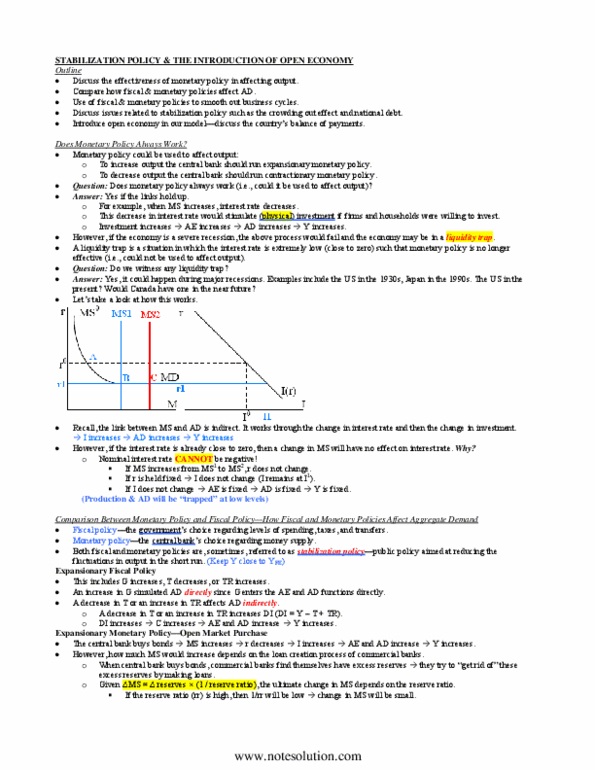

The role of the banking system how it generates money. N discuss the two types of banks commercial bank & central bank. N measures used by the central bank to affect money supply. There are two types of banks: commercial banks and central bank. N commercial banks are privately owned, profit-seeking institutions that provide a variety of financial services such as accepting. The link between monetary policy and the real side of the economy a revisit. deposits from customers and making loans and other investments. In canada, the banking industry is dominated by chartered banks. N chartered banks in canada include rbc, bmo, cibc, td-canada trust, and scotiabank. N chartered banks are subject to federal regulations and only until recently were required to hold reserves with the bank of canada (boc) against their deposit liabilities. The required reserve requirement was eliminated in 1994 but chartered banks still hold voluntary reserves with the boc.