ACT370H1 Lecture Notes - Dividend Yield

Document Summary

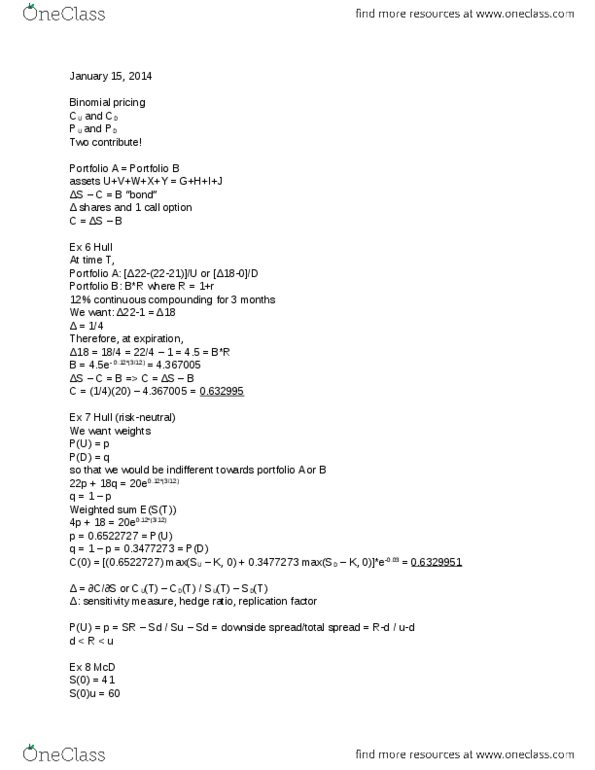

Compare to k [itm] s-k or k-s, [otm] 0. Take the terminal option values and probabilities and work backwards. Terminal value: expiration -> [call] max(s-k,0), [put] max(k-s,0) K = 21 u = 1. 1 d = 0. 9 r = 0. 12. T = 6/12 (2 periods of 3 months) p = 0. 6522727 = p(u) Cb = e-0. 12*(3/12) (0. 652*3. 2 + 0. 3478*0) = 0. 2025584 => value at point b. Ca = e-0. 12*(3/12) (0. 652*2. 2025584 + 0. 348*0) = 1. 282185 => value of call at t=0. K = 52 u = 1. 2 d = 0. 8 r = 0. 05. T = 2 (2 1-year periods) p = 0. 6281777 = p(u) Here the up event is still stock price rises . Volatility (brief preview) u = e(r- )h + h d = e(r- )h - h (from mcdonald book) = dividend yield of the stock = q (hull) h = length of our (short) time interval = t (hull)