ECO101H1 Lecture Notes - Lecture 9: Monopoly Price, Profit Maximization, Marginal Revenue

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

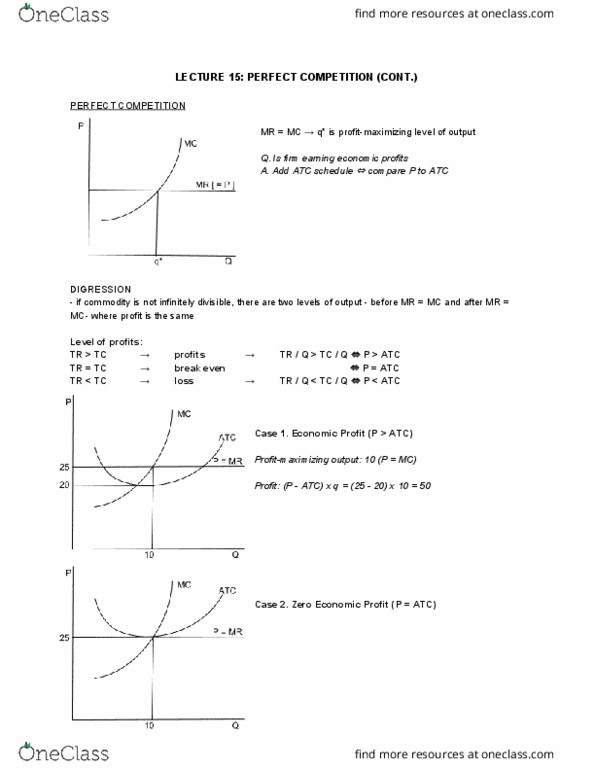

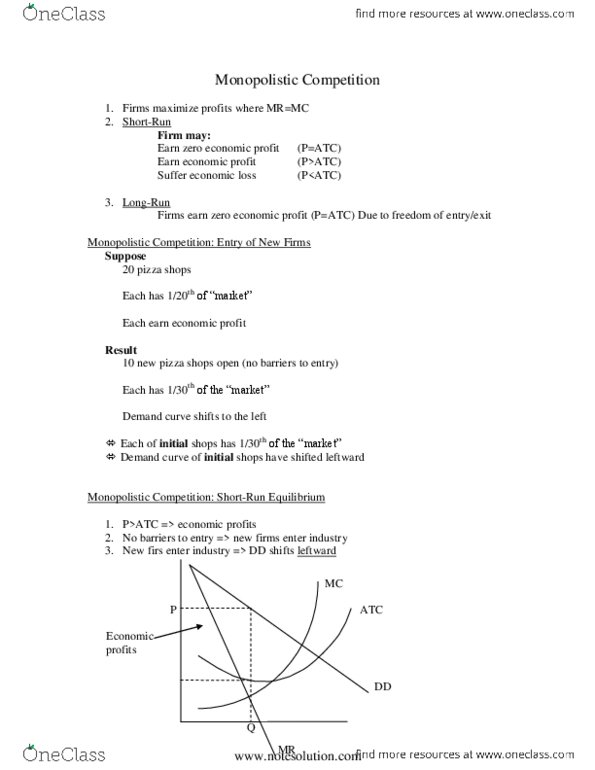

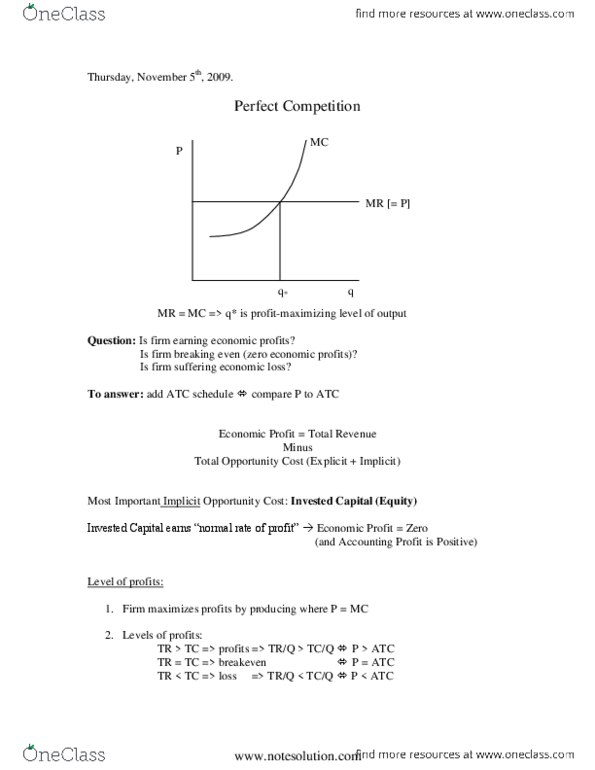

P = = mc = (minimum) atc. Demand increases, market price increases (from to ) Case 1: new firms have identical cost schedules as existing firms. In long run, p = = minimum (unchanged) atc. 10,000 old firms and 1000 new firms earn zero economic profits. Case (cid:1006): (cid:1005),(cid:1004)(cid:1004)(cid:1004) (cid:374)ew fir(cid:373)s results wages a(cid:374)d mc of all fir(cid:373)s by (cid:894)so atc of all fir(cid:373)s (cid:895) In the long run, p = = (minimum) atc of all firms. Price falls from short-term level () as new firms enter industry, but only to . In eco100, we will focus only on case 1: as shown by case 2, we need to track how (minimum) atc changes as new firms enter industry to identify long-run industry supply curve. Single seller (of product with no close substitutes) Barriers to entry: legal barriers (legal monopoly)