ECO102H1 Lecture Notes - Gross Domestic Product, Output Gap, Potential Output

45

ECO102H1 Full Course Notes

Verified Note

45 documents

Document Summary

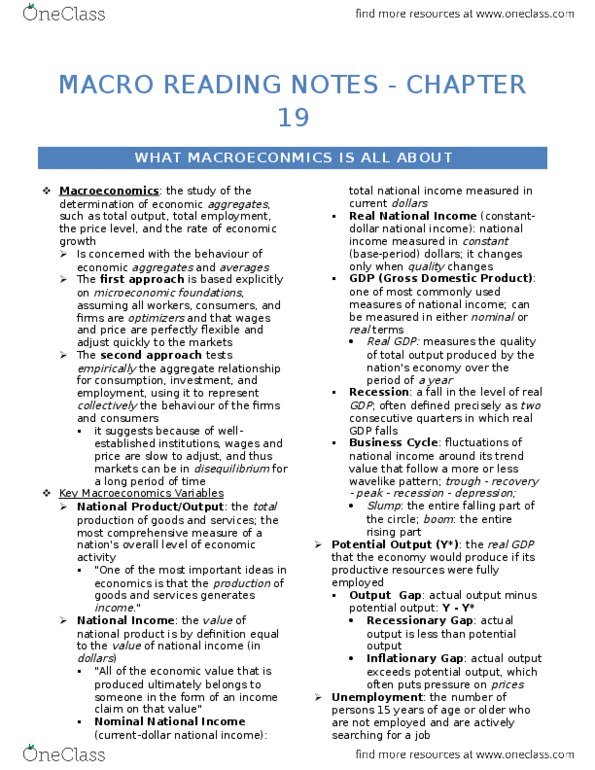

Macroeconomics: the study of the determination of economic aggregates, such as total output, total employment, the price level, and the real economic growth. These aggregates results from activities in many different markets and from the command behaviour of millions of different decisions maker. Studying aggregates may cause us to miss important differences but it focuses on retention on some important issue for the economy as a whole. Moments in economic aggregates matter for most individuals because they influence the help of the industries in which all worked and the prices of the goods that they purchase. Macroeconomics considered two different aspects of the economy: one is economists think about the short-run behaviour of macroeconomic variables such as output, employment, and inflation, and about how government policy can influence these variables. This concerns among other things, the study of business cycles. Second is economists also examine the long-run behavior of the same variables specially the long-run have of aggregate output.