ECO100Y1 Lecture Notes - Lecture 9: Perfect Competition, Demand Curve, Takers

Document Summary

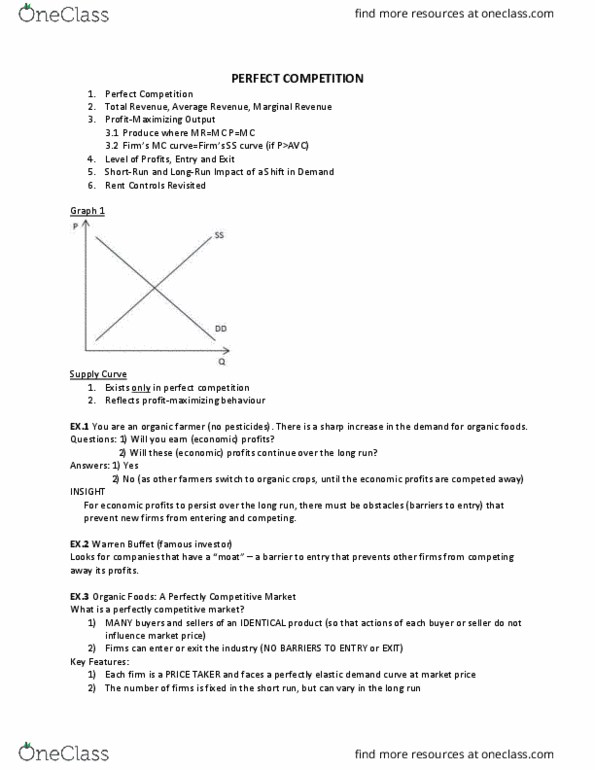

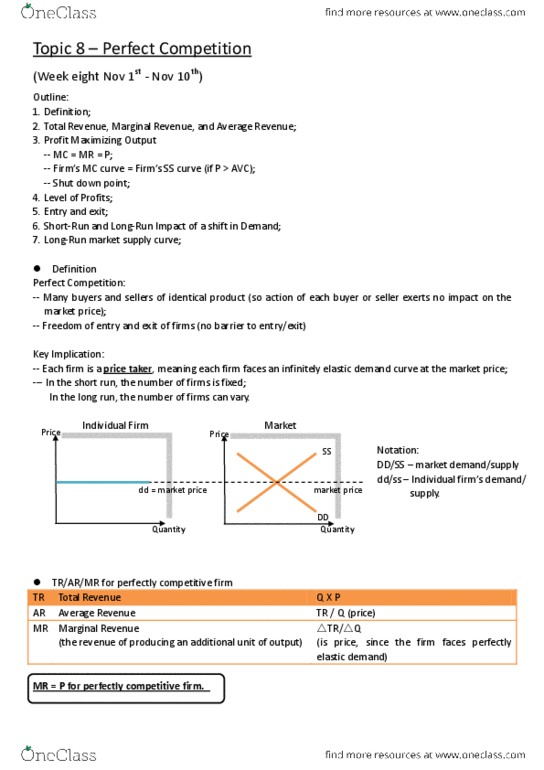

There is a sharp increase in the demand for organic foods. 2)no(as other farmers switch to organic crops, until the economic profits are competed away) For economic profits to persist over the long run, there must be obstacles(barriers to entry) that prevent new firms from entering and competing. 1)many buyers and sellers of an identical product (so that actions of each buyer or seller do not influence market price. 2)firms can enter or exit the industry (no barriers to entry or exit) 1)each firm is a price taker and faces a perfectly elastic demand curve at market price. 2)the number of firms is fixed in the short run, but can vary in the long run graph 2. Dd = market demand curve dd = firm"s demand curve. The price elasticity of demand faced by an individual coffee grower is closest to: Q p tr ar mr (p * q) (tr/q) (^tr/^q)