RSM225H1 Lecture : chapter 2

Document Summary

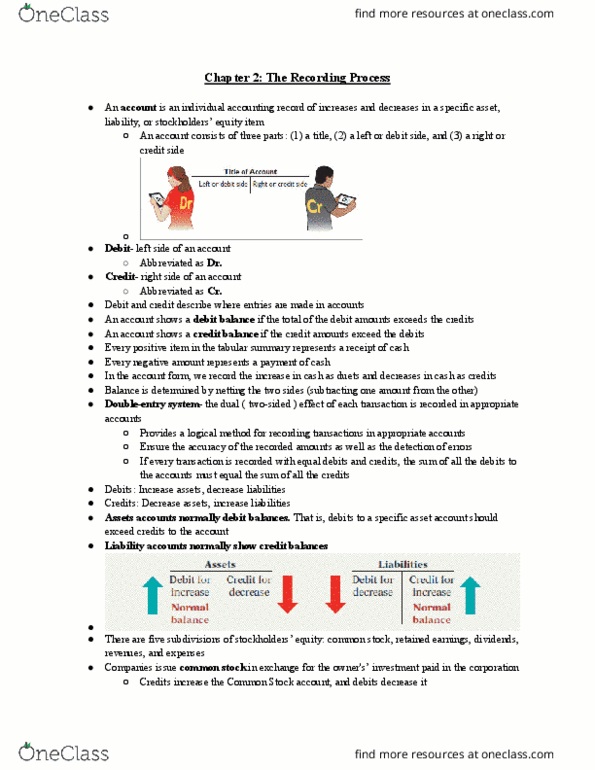

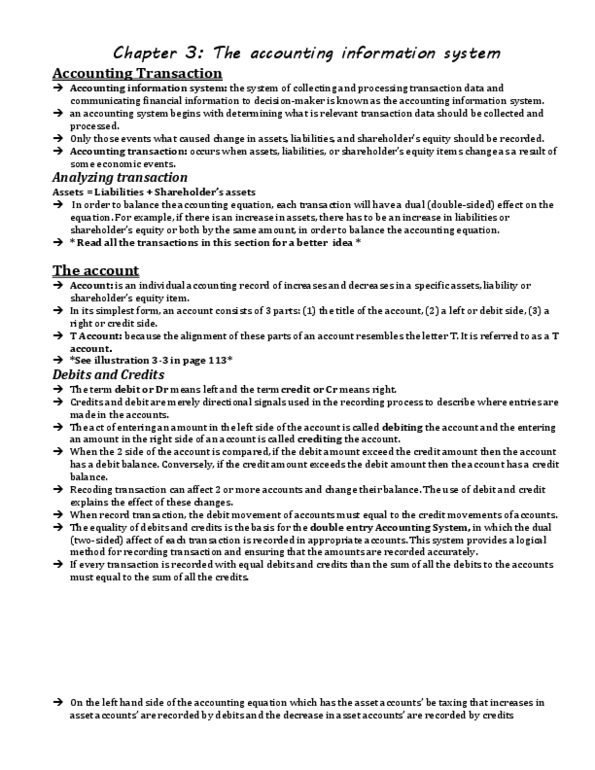

An account is an individual accounting record of increases and decreases in a specific asset, liability, or owner"s equity item. 1. 3 the positioning of these parts resembles the letter t, and therefore the account form is called a t account: debits and credits. 2. 2 in a double-entry system, equal debit and credit amounts are entered in the accounts for each transaction. Thus, the total debits will always equal the total credits. 2. 3 assets, drawings, and expenses are increased by debits and decreased by credits. 2. 4 liabilities, owner"s capital, and revenues are increased by credits and decreased by debits. Assets = liabilities + capital - drawings + revenues expenses: steps in the recording process. 3. 1 the basic steps in the recording process are: 3. 1. 1 analyse each transaction in terms of its effect on the accounts. 3. 1. 2 enter the transaction information in a journal (book of original entry).