ECON 1100 Lecture Notes - Lecture 18: Perfect Competition, Demand Curve, Takers

4 Sep 2019

School

Department

Course

Professor

Document Summary

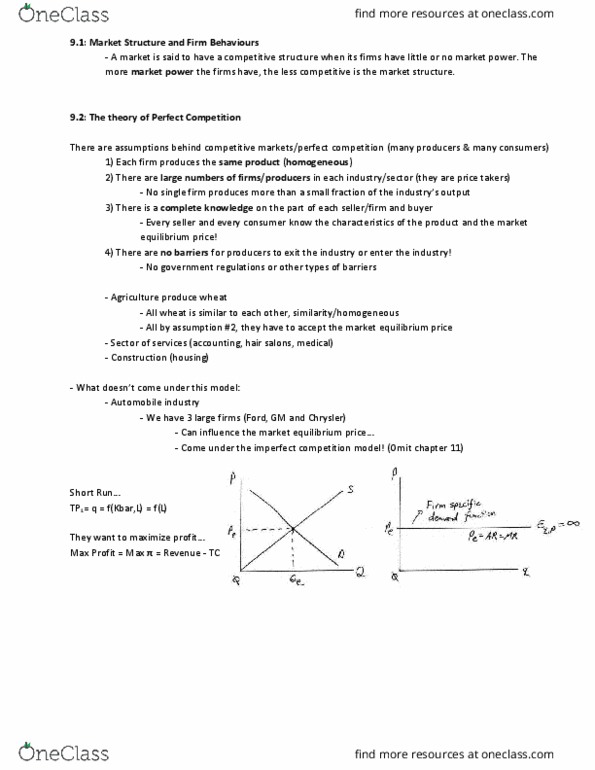

Theory of perfect competition: in perfect competition firms are price takers, there is freedom of entry and exit: The demand curve facing a perfectly competitive firm is horizontal. If price > pc, the consumer is willing to buy nothing. If the price is less than or equal to ( < ) pc, the consumer is willing to buy positive amounts of q. Variations in firms output have no effect on the price. The industry of market demand curve remain downward sloping. Revenue firms receive from the sales of their product. The change in the firm"s total revenue with respect to a change in quantity. From the above table, we can observe that as a result of the firm changing its output, neither mr or ar vary with output. If the market price is unaffected by variations in the firm"s output, the demand curve, ar curve, and mr curve all coincide in the same horizontal line.