Actuarial Science 2553A/B Lecture Notes - Lecture 4: Discounting, Interest, Current Yield

85 views21 pages

11 Oct 2016

School

Department

Professor

Document Summary

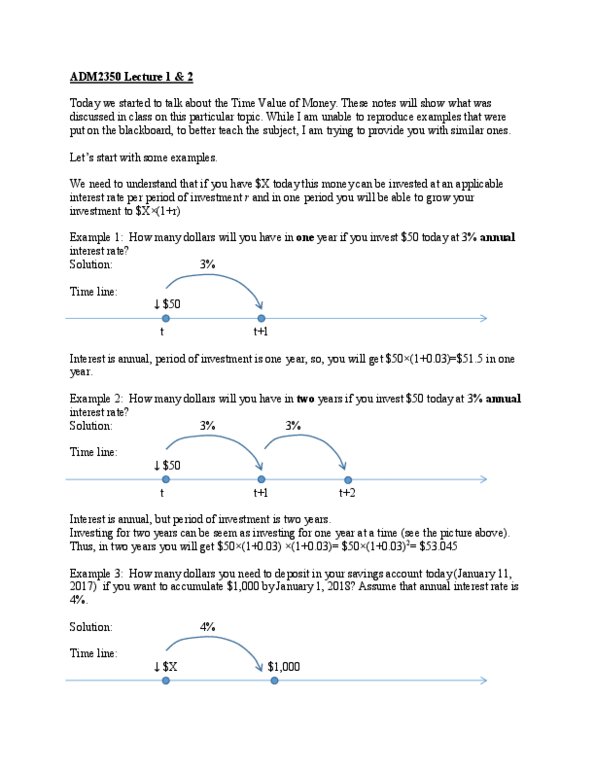

We know that p invested today at a rate of interest i, will accumulate to s in t-years" time. A(0) invested today will grow to a(t) after t-years, and today will grow to a(t) in t-years. To answer the above questions, we need to calculate what is called the present value or discounted value of a future sum. (i) compound interest. A(t) = a(0) a(t) = a(0) (1 + i)t. Thus, p = a(0) = s(1 + i) t and p would be called the present value or discounted value of s. Actuaries commonly use the following notation for the discount factor: 1 i = (1 + i) 1 v = This notation will be more useful in chapter 3. As interest rates go up, present values go down. Ordinary calculations: accumulated value exact < a. v ordinary, present value exact > pv ordinary. Simple interest: av under ci > av under si, pv under ci < pv under si.