Management and Organizational Studies 3367A/B Lecture Notes - Lecture 7: Rubber Stamp, Accounts Receivable, Purchase Order

8 Mar 2018

School

Department

Professor

Document Summary

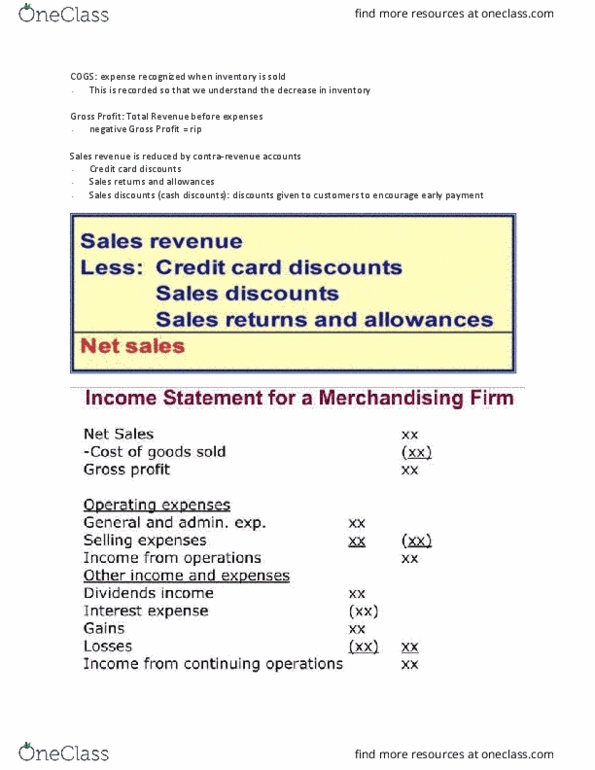

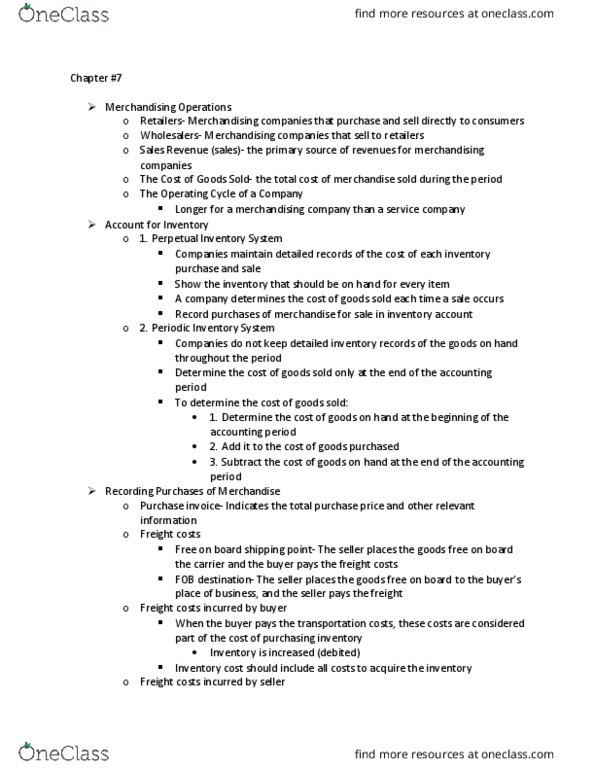

A refund is processed when a customer returns an item of merchandise purchased from the store. Purchase price is returned to the customer. Fictitious refunds: fraudster takes cash from the register in the amount of the false refund, debit is made to the inventory system showing that the merchandise has been returned to the inventory. Overstated refunds: fraudster overstates the amount of a legitimate refund and skims the excess money, customer is paid the actual amount owed for the returned merchandise and the excess is kept by the fraudster. Credit card refunds: refu(cid:374)ds appea(cid:396) as (cid:272)(cid:396)edits to the (cid:272)usto(cid:373)e(cid:396)"s (cid:272)(cid:396)edit (cid:272)a(cid:396)d (cid:396)athe(cid:396) tha(cid:374) as dash disbursements, perpetrator does not have to physically take cash from the register, refu(cid:374)ded to the pe(cid:396)pet(cid:396)ato(cid:396)"s (cid:272)(cid:396)edit (cid:272)a(cid:396)d. Also generate a disbursement from the register. Copy of (cid:272)usto(cid:373)e(cid:396)"s (cid:396)e(cid:272)eipt is atta(cid:272)hed to the (cid:448)oid slip. Rubber stamp approvals allow the fraud to succeed. Fraudsters typically do not make any effort to conceal the shrinkage.