Management and Organizational Studies 3370A/B Lecture Notes - Lecture 8: Standard Cost Accounting, Purchasing Manager, Variable Cost

23 Nov 2016

School

Department

Professor

Document Summary

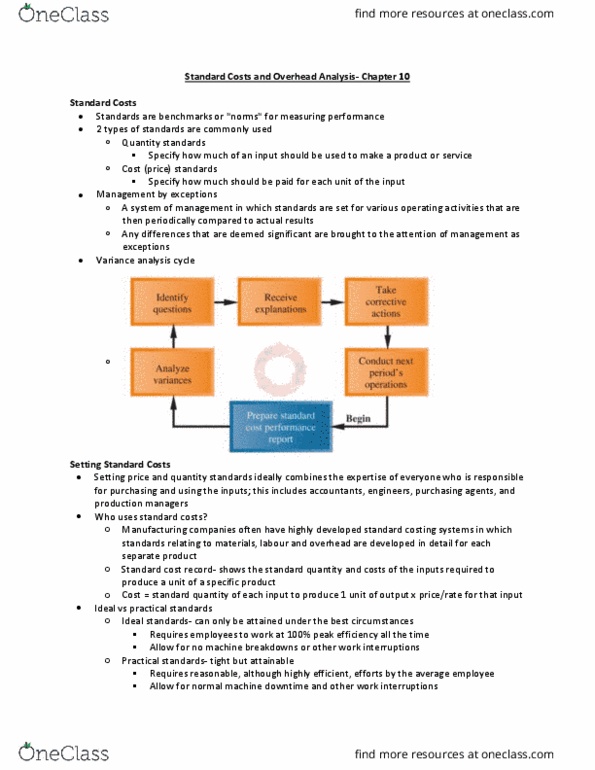

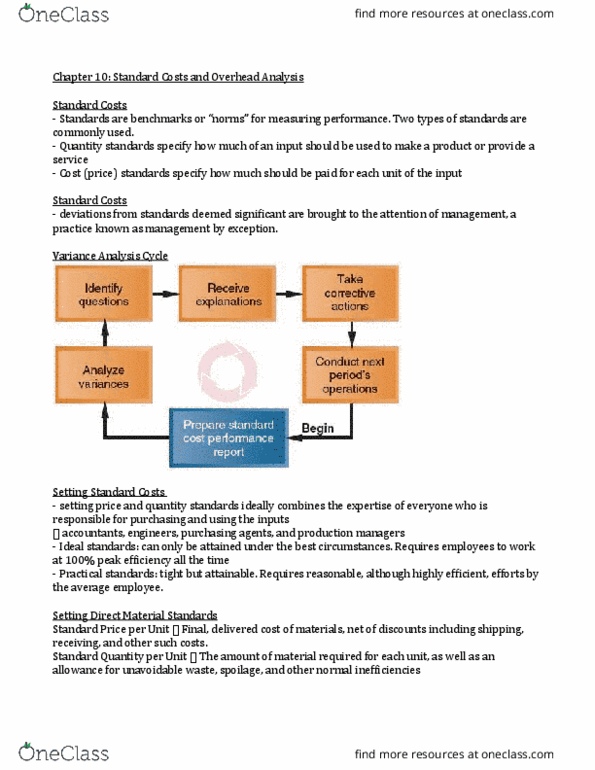

Standard costs benchmarks or norms for measuring performance. Management by exception: deviations from standards deemed significant are brought to the attention of management. Setting price and quantity standards ideally combines the expertise of everyone who is responsible for purchasing and using the inputs: accountants, engineers, purchasing agents, and production managers. Ideal standards: can only be attained under the best circumstances. 100% peak efficiency all the time: unrealistic. Practical standards: tight but attainable; requires reasonable, although highly efficient, efforts by the average employee. Standard price per unit final, delivered cost of materials, net of discounts including shipping, receiving, and other such costs. Standard quantity per unit the amount of material required for each unit, as well as an allowance for unavoidable waste, spoilage, and other normal inefficiencies. Standard rate per hour - the labour rate that should be incurred per hour of labour time, including. Employment insurance, employee benefits, and other labour costs.