Management and Organizational Studies 1021A/B Lecture Notes - Lecture 2: Deferred Income, Current Liability, Accounts Payable

10 Feb 2017

School

Department

Professor

21

MOS 1021A/B Full Course Notes

Verified Note

21 documents

Document Summary

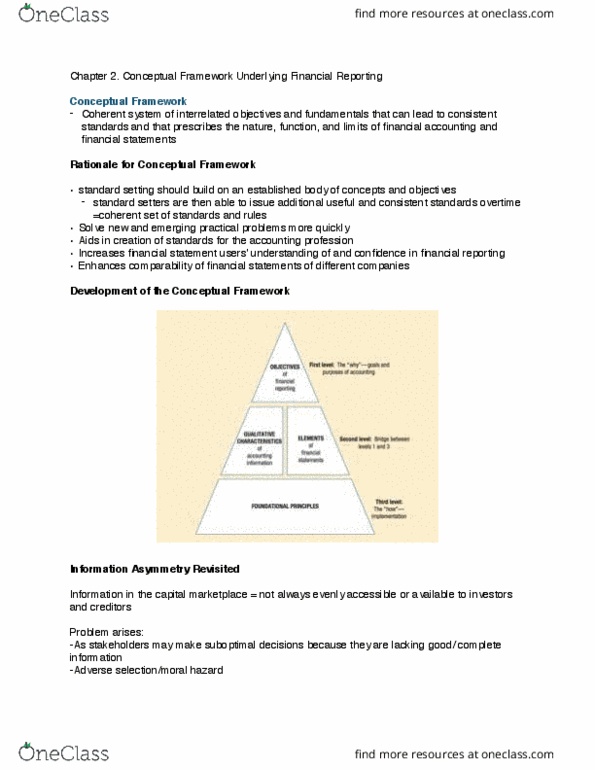

A conceptual framework: is like a constitution: it is a coherent system of interrelated objectives and fundamentals that can lead to consistent standards and that prescribes the nature, function and limits of financial accounting and financial statements. To be useful, standard setting should build on an established body of concepts and objectives. Aids in creation of standards for the accounting profession. I(cid:374)(cid:272)(cid:396)eases fi(cid:374)a(cid:374)(cid:272)ial state(cid:373)e(cid:374)t use(cid:396)s(cid:859) u(cid:374)de(cid:396)sta(cid:374)di(cid:374)g of a(cid:374)d (cid:272)o(cid:374)fide(cid:374)(cid:272)e i(cid:374) financial reporting. Enhances comparability of financial statements of different companies. The framework is a reference of basic accounting theory for solving new and emerging practical problems of reporting. According to the conceptual framework, the objective of financial reporting is to communicate information that is: Useful to investors, creditors, and other users. To be relevant, accounting information must be capable of making a difference in a decision. If a piece of information has no impact on a decision, it is irrelevant to that decision.