Management and Organizational Studies 1023A/B Lecture Notes - Lecture 2: Income Statement, Historical Cost, Going Concern

25 Oct 2017

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

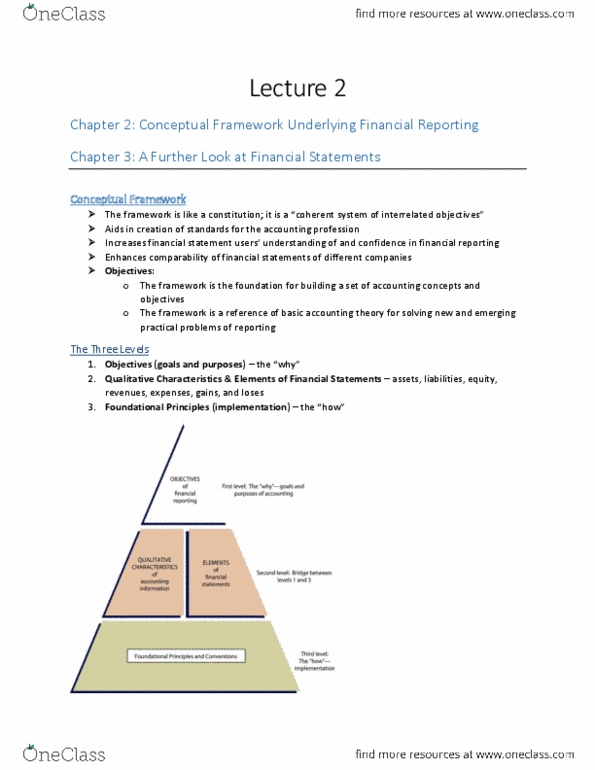

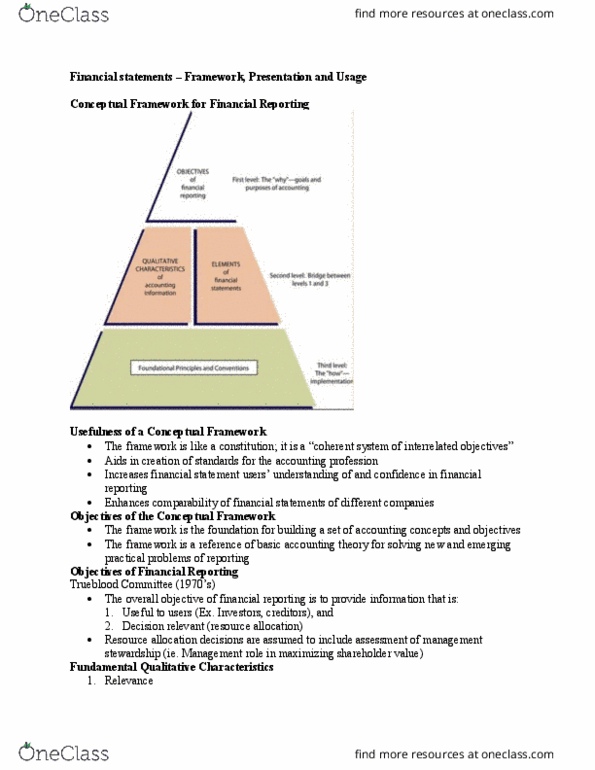

Trueblood committee (1970"s: the overall objective of financial reporting is to provide info that is, useful to users (i. e. investors, creditors, decision relevant (resource allocation) Resource allocation decisions are assumed to include assessment of management stewardship(i. e. management role in maximizing shareholder value) Fundamental qualitative characteristics: relevance, makes a difference in a decision, has predictive and feedback, representational faithfulness (reliable, complete, neutral, free from material error, substance over form (legal) It is not always possible to have all fundamental and enhancing qualitative characteristics trade-offs happen when one qualitative characteristic is scarified for another. Materiality: how important the info is if it changes a users decision. If leaving or including info would influence/change the judhement of a reasonable person, then that info is considered material: quantitative guidelines for materiality -professional judgement. I. e. company x makes 80 bil net profit, there is a error. This is not material bc it does not really matter since it the error is so small.