Management and Organizational Studies 3361A/B Lecture 18: Chapter 18 Lecture Slides.docx

10 Apr 2015

School

Department

Professor

Document Summary

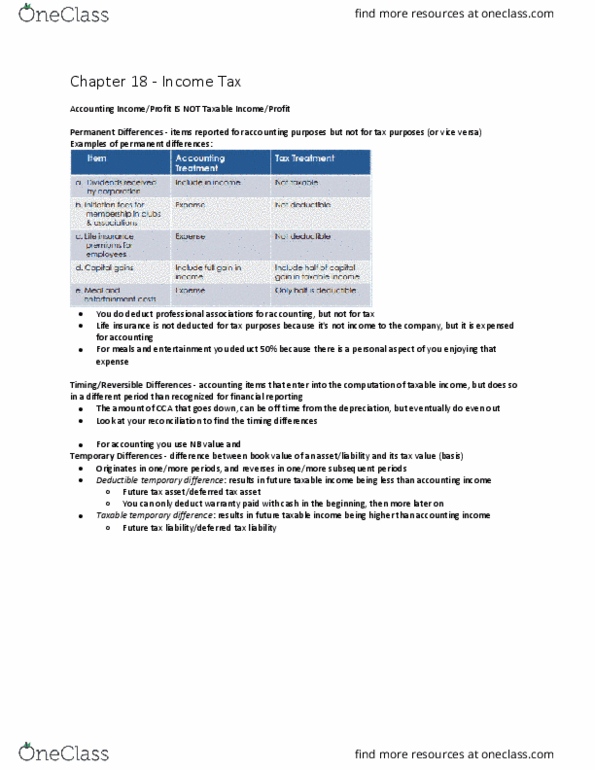

Accounting for income taxes: accounting income/profit taxable income/profit, accounting is gaap based and has accruals, taxable there are tax regulations, the tax man only lets you deduct what you paid in cash, the difference between accounting income/profit and taxable income/profit arises due to, permanent differences, temporary differences. If everyone in the company is invited they can deduct 100%: example: 50% capital gains, if i buy and sell shares and make k i can deduct 50% that won"t be taxed, dividends received from canadian corporations, dividends received from canadian corporations can be deducted because technically that money has already been taxed. Timing/reversible differences: accounting items that enter into the computation of taxable income but do so in a difference period than recognized for financial reporting, represent change in a temporary difference in the period, examples, depreciation/cca, warranty costs (cash basis for tax, installment sales income, bond discount/premium amortization.