Management and Organizational Studies 3370A/B Lecture 3: MOS 1023 LECTURE 3 notes.docx

27 Apr 2015

School

Department

Professor

Document Summary

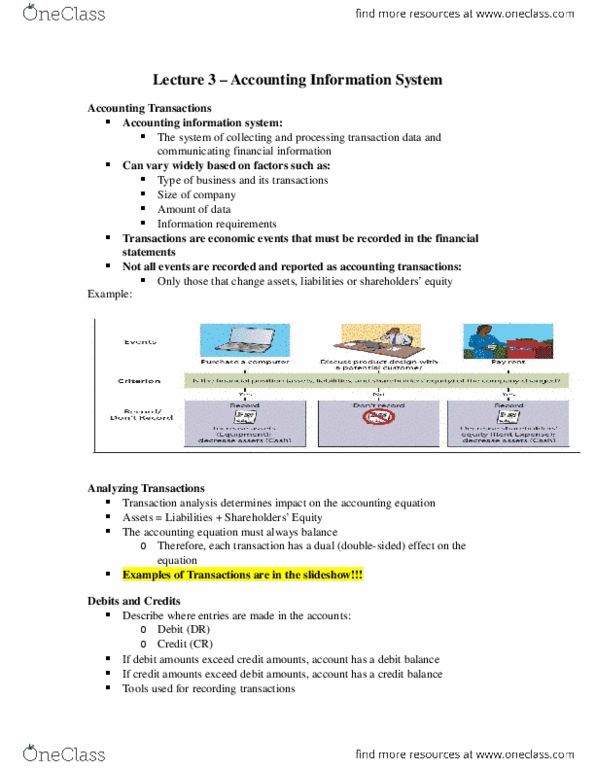

Accounting transactions changes in a l s. e: only certain relevant transaction data should be collected and it"s the events that cause changes in assets liabilities or shareholders equity (cid:224)analyzing transactions / summary of transactions, each transaction must be analyzed for its effect on the three primary components of the accounting equation assets = liabilities + shareholders equity the two sides of the equations must always be equal. The account: an individual accounting record of increases and decreases in a specific asset, liability or shareholders equity, consists of three parts, the title of account, a left or debit side, a right or credit side. Normally show credit balances: because assets are on the opposite side of liabilities and shareholders equity increases/ decreases will be opposite of l/s. e (cid:224) total amount of debits always equals total amount of credits to stay balanced, common shares exchange for shareholders investment, retained earnings is amount shareholders equity has accumulated.