BU121 Lecture Notes - Cash Conversion Cycle, Asset, Corporate Finance

Document Summary

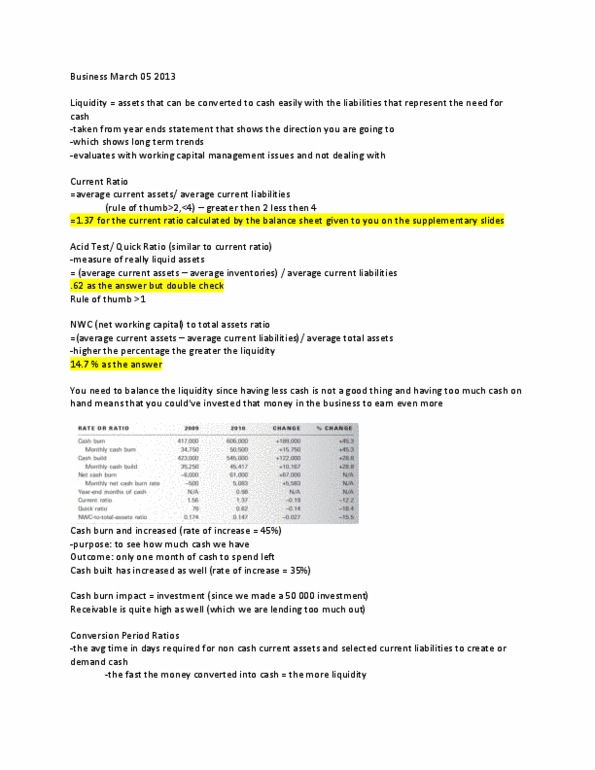

Conversion period ratios: measure average time in days required for non-cash current assets and selected current liabilities to create/demand cash. Faster assets can be converted into cash, greater the liquidity: tells you the actual time it"s taking, operating cycle: measures time it takes to purchase raw materials, assemble a product, book the sale and collect on it. Want to balance them: cash conversion cycle = inventory to sale + sale to cash - purchase to payment conversion period, number of days of operation that must be externally financed. Number of days that you don"t have enough cash: should be as close to 0 as possible. Interest (cheaper than dividends but higher return & risk) vs. dividends (not obligated to pay) Expense for borrowing is less than equity because of tax savings (lower cost of capital, return is higher: risk/return tradeoff. Higher the return, higher the risk: control vs. legal recourse.