BU127 Lecture 5: Chapter 5

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

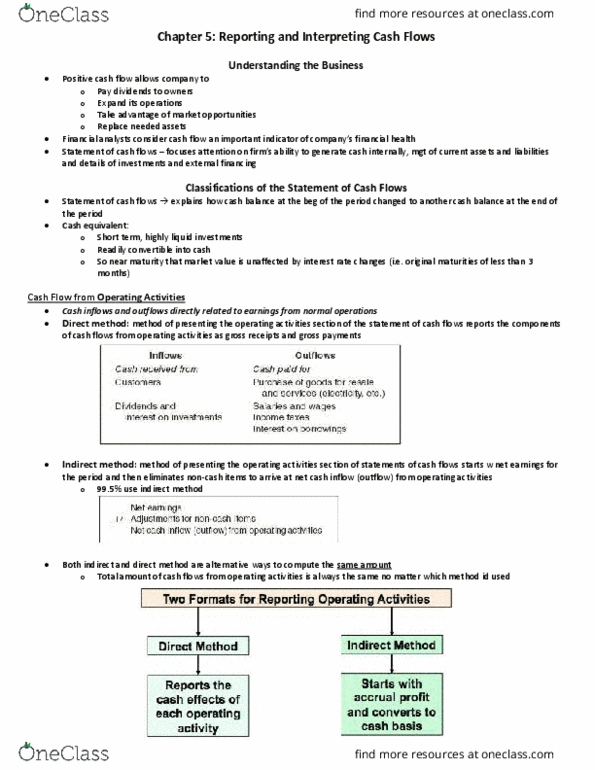

Positive cash flows permit a company to: pay dividends to owners, take advantage of market opportunities, expand its operations, replace needed assets. Financial analysts consider cash flow an important indicator of a company"s financial health. Cash equivalents: short term high liquid investments, readily convertible into cash, market value is unaffected by interest rate changes. Operating activities: cash inflows and outflows directly related to earnings from normal operations. Investing activities: cash inflows and outflows related to the acquisition or sale of productive facilities and investments in the securities of other companies. Financing activities: cash inflows and outflows related to external sources of financing for the enterprise. The direct method of presenting the operating activities section of the statement of cash flows reports components of cash flows from operating activities as gross receipts and gross payments: The indirect method of presenting the operating activities section of the statement of cash flows adjusts profit to compute cash flows from operating activities.