BU127 Lecture Notes - Lecture 2: Deferral, Accounts Payable, Current Asset

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

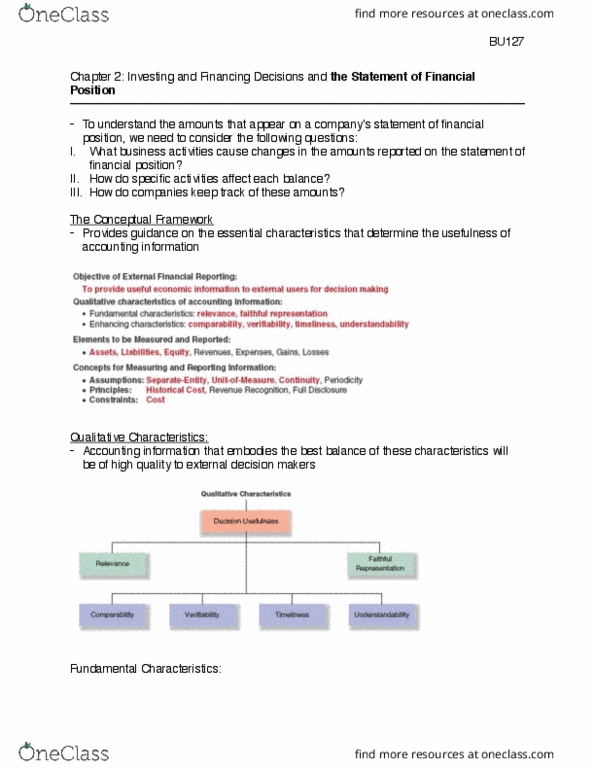

Lecture 2: investing & financing decisions & the statement of financial. Assets used/ turned in to cash within one year. Inventory is always considered a current asset, regardless of time needed to produce & sell. Examples: cash, short-term investments, accounts receivable, prepaid expenses (expenses paid in advance use, other current assets. Be turned in to cash over a period longer than a year. Examples: property & equipment (at cost less depreciation, financial assets, goodwill, other (misc. assets) Present debts/obligations that result from past transactions that will be paid in cash (or other current assets) Debts/obligations that have maturities that extend beyond one year from statement of financial position date. Additional note: prepaid expense or prepayment is not an expense, it is an asset. Refers to the amounts paid in advance for future benefits. Refers to amounts that have been paid in: deferred revenue or unearned revenue is not a revenue, it is a liability.