BU227 Lecture : Chapter 3 Operating Decisions and the Income Statement

Document Summary

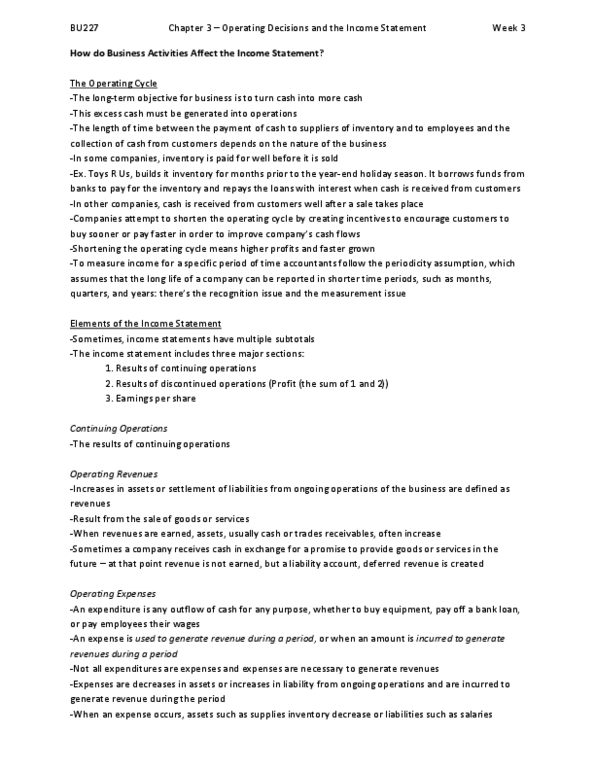

3: operating decisions and the income statement income statement provides the basis for comparing analysts" projections to results of operations. Not a snapshot this is a report over a period of time. Operating (cash-to-cash) cycle: time it takes for a firm to pay cash to suppliers, sell goods/services. Lt goal = turn cash into more cash, by operations; not by borrowing or selling non-current assets to customers, and collect cash from customers the cycle depends on the nature of the business. Short-term debt financing: many businesses pay suppliers/workers before they receive cash from customers, so they seek st financing. When they receive cash from customers, they pay off liabilities. In order to improve the company"s cash flows, firms try to shorten the operating cycle by creating incentives for customers to buy sooner and pay faster higher profits, faster growth. Periodicity assumption: long life of a company can be reported in shorter periods.