BU247 Lecture Notes - Cost Driver, Profit Margin, Standard Cost Accounting

Document Summary

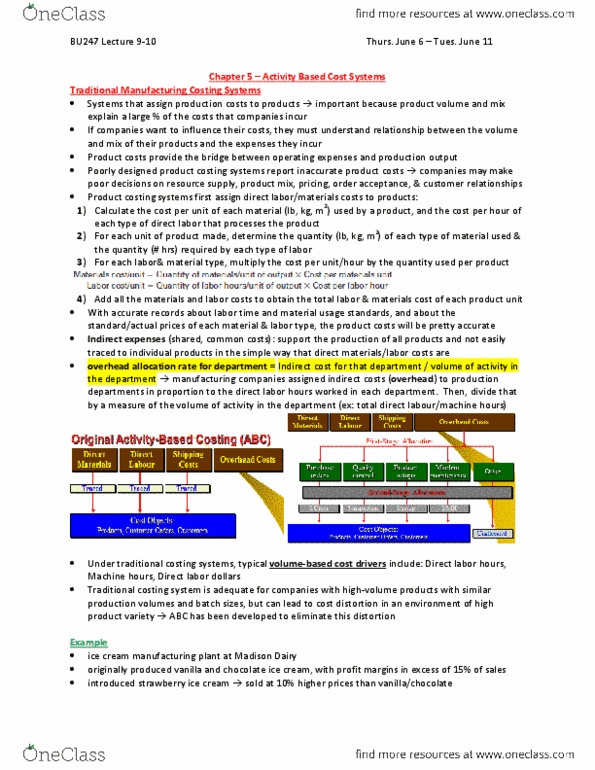

Systems that assign production costs to products important because product volume and mix explain a large % of the costs that companies incur. If companies want to influence their costs, they must understand relationship between the volume and mix of their products and the expenses they incur. Product costs provide the bridge between operating expenses and production output. Poorly designed product costing systems report inaccurate product costs companies may make poor decisions on resource supply, product mix, pricing, order acceptance, & customer relationships. With accurate records about labor time and material usage standards, and about the standard/actual prices of each material & labor type, the product costs will be pretty accurate. Indirect expenses (shared, common costs): support the production of all products and not easily traced to individual products in the simple way that direct materials/labor costs are. Then, divide that by a measure of the volume of activity in the department (ex: total direct labour/machine hours)