BU352 Lecture Notes - Capital Asset, International Traffic In Arms Regulations, European Cooperation In Science And Technology

CHAPTER SEVEN - CAPITAL GAINS: PERSONAL

(Div B, Subdiv c, S38-55)

HISTORY

Prior to 1972 capital gains were not taxed in Canada and capital losses could not be claimed.

The portion (inclusion rate) of a capital gain or loss which is taxable/deductible has changed

since then. [calendar 1972 to 1987 => 50%; calendar 1988 to 1989 => 66.67%; calendar 1990 to

Feb 27, 2000 => 75%; Feb 28 to Oct 17, 2000 => 66.67%; Oct 18, 2000 to present => 50%]

Since 1972, each disposition of capital property requires a separate calculation of taxable capital

gain or allowable capital loss. Section 3(b) requires that allowable capital losses be offset against

taxable capital gains, except as discussed below for PUP (including LPP) and ABILs. If the net

result of all current year capital dispositions is a taxable capital gain, this amount is included in

Division B income. If the net result is an allowable capital loss, this amount is not deductible

currently since allowable capital losses can ONLY BE DEDUCTED AGAINST taxable capital

gains. (A net allowable capital loss for the current year can be carried over to other years under

Division C, as will be discussed in chapter 10.)

TERMINOLOGY

Capital property includes any depreciable property, and any other property that would result in a

capital gain or loss on disposition (based on the common-law principles above.)

Rules related to the computation of net taxable capital gains refer to 3 classifications of

properties: Personal Use Property (property acquired for personal use and enjoyment of the

taxpayer), Listed Personal Property (specific collectibles not expected to depreciate represent a

specific subset of PUP) and Other Capital Property (the default classification which includes

capital property acquired to generate income from business or property)

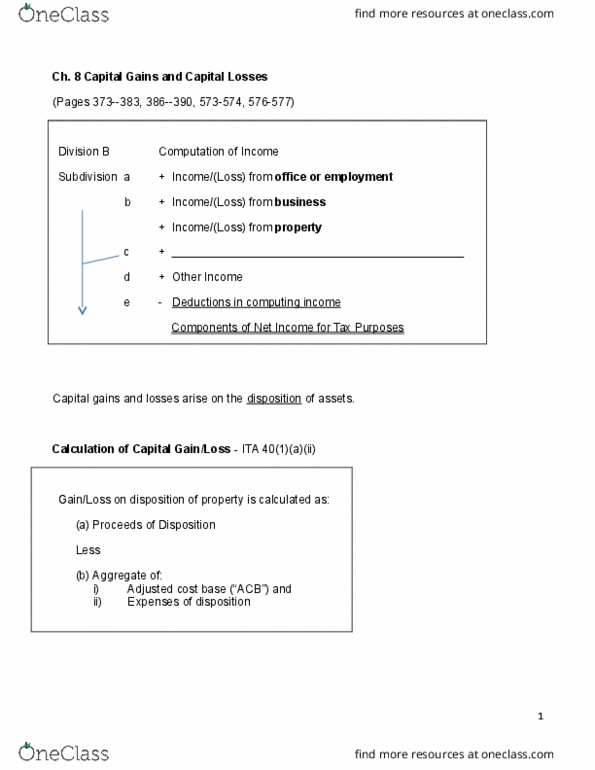

Proceeds of disposition

less: Adjusted cost base

less: Costs of disposition

= Gain or Loss

less: Exemptions (S40 Reserve for amounts not yet due; Principal residence exemption)

= Capital Gain or Capital Loss

times: Current year inclusion rate

= Taxable Capital Gain or Allowable Capital Loss.

Capital gains or losses are only computed at the time of disposition. For tax purposes

dispositions include sales, but can also be “deemed” on change in use, death of the taxpayer,

emigration of the taxpayer from Canada and on gifting of the asset to another taxpayer. ACB

computations begin with accounting “laid-in cost” but may require adjustment for tax purposes in

accordance with sections 52 and 53 and the ITAR’s (for assets acquired prior to 1972). The

applicable inclusion rate is determined based on the date of DISPOSITION of a capital asset.

find more resources at oneclass.com

find more resources at oneclass.com

The disposition of Depreciable Capital Property can give rise to capital gains, but can never

result in a capital loss! This is due to the fact that a “loss in value” would be given a 100%

deduction under the CCA system. (To allow a capital loss in addition, would be double counting

this cost for tax purposes.)

CAPITAL GAINS DEDUCTION

The general capital gains deduction allowing resident individuals (not corporations) to earn in

their lifetime $100,000 of capital gains tax free, existed between 1985 and 1994. The deduction

was claimable only in the year of a capital disposition which gave rise to a capital gain. In 1994 a

final election to use any unused portion of the lifetime limit against unrealized gains which could

be supported by FMV appraisals was allowed. The benefit of the election was to increase the

ACB of capital assets which had increased in value but had not yet been subjected to a

disposition. This election may still be relevant in tax preparation today, where a taxpayer

disposes of property (say real estate) which was acquired prior to 1994 and on which an election

had been made.

A further capital gains deduction allowing resident individuals to earn in their lifetime $835,716

less any prior claims made under the general deduction above) of capitals gains tax free on the

sale of qualified Small Business Corporation shares and qualified farming or fishing properties

only, still exists today.

This deduction again represents a tax incentive to motivate investors to invest in Canadian small

business and to assist farming & fishing operations.

PERSONAL USE PROPERTY

Property acquired primarily for personal use, as opposed to income earning use, most commonly

results in capital losses on disposition. These losses are deemed to be personal or living costs and

may not be used to offset capital gains for tax purposes. However, if a capital gain results on

disposition it is taxable.

For purposes of capital gains calculations, the proceeds and the ACB of PUP is deemed to be the

greater of actual proceeds (or ACB) and $1,000. This effectively excludes “smaller” PUP gains

from taxation.

LISTED PERSONAL PROPERTY

This subset of PUP includes works of art, jewellery, rare books, stamps & coins.

Capital losses on disposition of LPP may be used to offset capital gains from LPP only.

Similarly, net capital losses of LPP in any year may be carried back up to 3 years and forward up

to 7 years to offset net LPP capital gains, under Division B.

find more resources at oneclass.com

find more resources at oneclass.com

PRINCIPAL RESIDENCE EXEMPTION

Gains on the disposition of a Principal Residence may be exempted by “Designating” the

residence as such for specific years, and thus claiming the exemption.

Principal residence - any housing unit owned by the taxpayer outright or jointly and ordinarily

inhabited (at least 24 hours in a year) by the taxpayer, his spouse or child at any time in the year.

- normally includes house and up to ½ hectare of surrounding land. (May include more than ½

hectare if land necessary to “use and enjoyment”. See Folio S1-F3-C2)

Designation - only necessary to designate post-1971 calendar years, in the year of disposal.

- since 1981, only one property may be designated by any taxpayer’s family unit (includes

spouses and unmarried minor children) in a given tax year. (1972 - 1980 one designation per year

possible per taxpayer.)

- form T2091, exemption calculation, need only be filed if some portion of gain on disposition of

residence sold remains taxable.

- taxpayer must be resident in Canada for tax purposes during any calendar year which is

designated.

Exemption formula = (1 + # of calendar years designated)/(# of calendar years in which property

owned) x gain.

Note: The exemption for principal residence can never exceed the gain to create say, a loss.

Therefore, there is no benefit to designating all years of ownership.

Algorithm to maximize the principal residence exemption where more than one eligible

residence is owned:

1 - Calculate the gain per year for each eligible residence.

2 - Exclude from consideration any years of ownership which have previously been designated

on prior disposition of other principal residences.

3 - Allocate any “no-option” years to the only eligible residence.

4 - Allocate the minimum years necessary to maximize the exemption for each property starting

from the highest “gain per year” to lowest gain per year.

5 - Check if any property has not been designated at all, and if the total exemption can be

improved by designating it for at least one year and reducing the designation of another property.

CHANGE IN USE OF PROPERTY - When a taxpayer changes the use of property from

personal use to income earning use (business, property, employment) or vice versa, there is a

deemed disposition at fair market value. This has potential negative tax consequences in terms of

recapture and capital gains without any actual proceeds. The same property is deemed reacquired

immediately thereafter at the same value for purposes of ACB determination. For purposes of

addition to the appropriate CCA class, the cost of the property is restricted to the original cost of

the property before change in use, plus the taxable capital gain recognized on change in use.

(Since only 50% of any capital gain is taxed, the taxpayer should only expect an increase in cost

for CCA purposes equal to this tax paid amount.)

For personal use property only, a taxpayer may elect under S45(2) to defer the capital gain

triggered on a change to income earning use, until such time as he or she disposes of the asset

(actual or deemed) or rescinds the election. However, the taxpayer is not able to claim CCA on

the asset used to earn income as long as the election is in effect. (This election is NOT available

where the initial use was income producing and the change is to personal use.)

find more resources at oneclass.com

find more resources at oneclass.com