BU387 Lecture Notes - Lecture 2: Conceptual Framework, Financial Statement, Income Statement

Document Summary

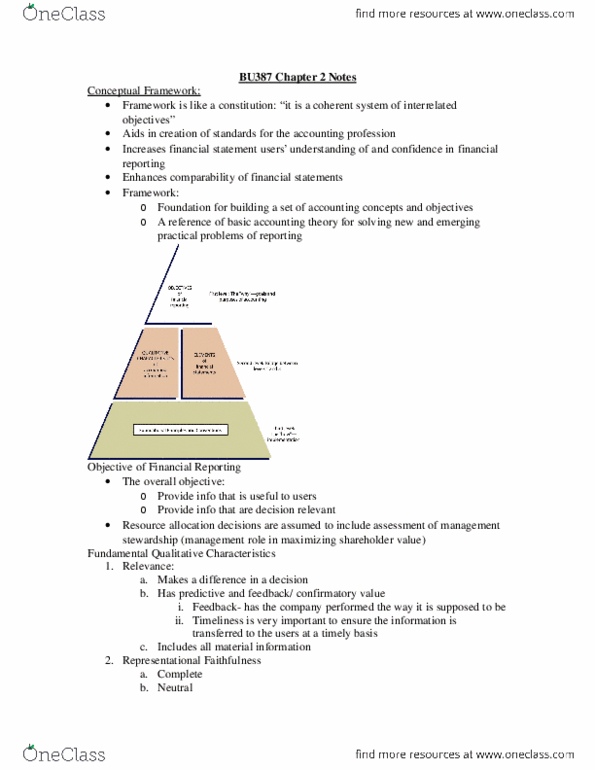

Chapter 2 conceptual framework underlying financial reporting. Conceptual framework: conceptual framework - a system of interrelated objectives and fundamentals that can lead to consistent standards and that prescribes the nature, function, and limits of financial accounting and financial statements, 1. ) Why is a conceptual framework necessary: to be useful, standard setting should build on an established body of concepts and objectives. Useful and consistent standards can be additionally added over time. The following diagram shows an overview of a conceptual framework. At the first level, the objectives ide(cid:374)tif(cid:455) a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g"s goals and purposes: these are the (cid:272)o(cid:374)(cid:272)eptual fra(cid:373)e(cid:449)ork"s (cid:271)uildi(cid:374)g (cid:271)lo(cid:272)ks. At the second level are the qualitative characteristics that make accounting information useful and the elements of financial statement (assets, liabilities, equity, revenues, expenses, gains and losses). At the third and final level are the foundational principles used in establishing and applying accounting standards. First level: the (cid:862)(cid:449)h(cid:455)(cid:863) goals and purposes of accounting. Second level: bridge between levels 1 and 3.