BU387 Lecture Notes - Lecture 5: Income Statement, Retained Earnings, European Cooperation In Science And Technology

Document Summary

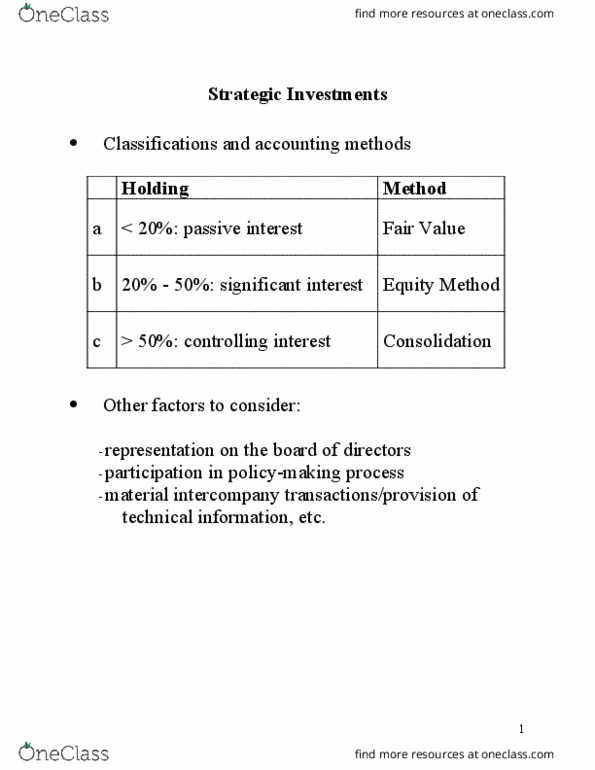

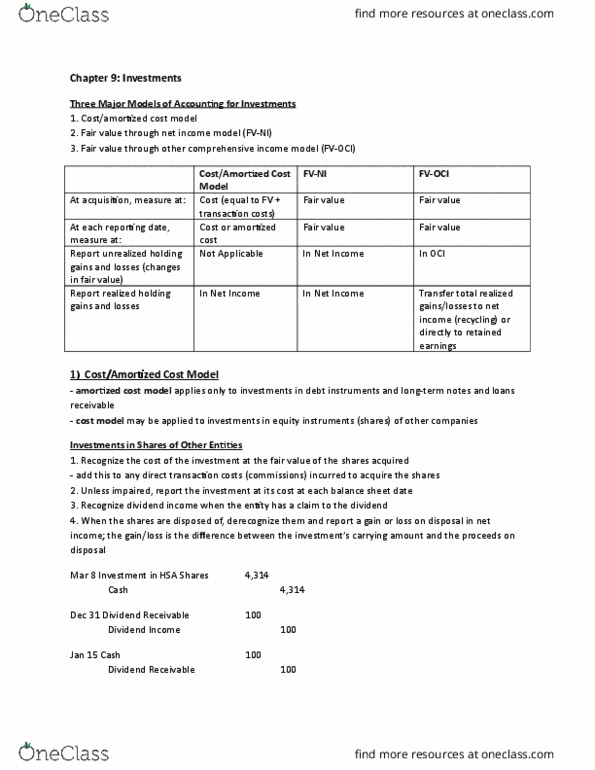

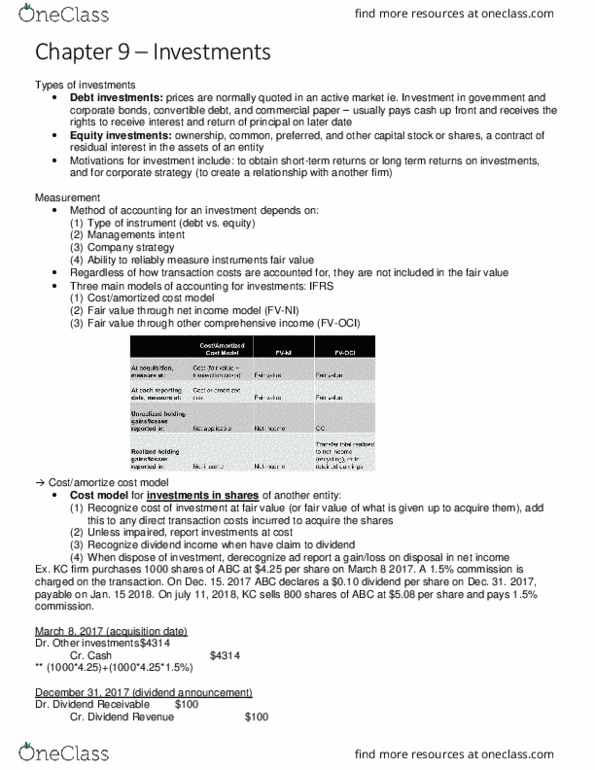

Decrease the discount and increase the bond. Net carrying value of bond x interest rate = interest income. Difference between the coupon and interest income = discount. If you have a significant influence on the board of directors you must account for these in a different manner. We account for those holdings if it is less than 20 percent. Use cost method if its < 20 % If the method is 50 % > consolidation method. Equity method is 20 % - 50 % - significant holding but not owner. Recognize that investment by cost unless it doesn"t recognize fair market value. This will become your carrying value of the investment. Acquire 5 % of investment (no significant influence) This is how much you would buy the investment for you would take the fair market value of abc the s/e at market value and multiply by 0. 3 (or percentage ownership)