ACTG 2011 Lecture Notes - Lecture 5: Accounts Payable, Cash Flow, Income Statement

Document Summary

Get access

Related Documents

Related Questions

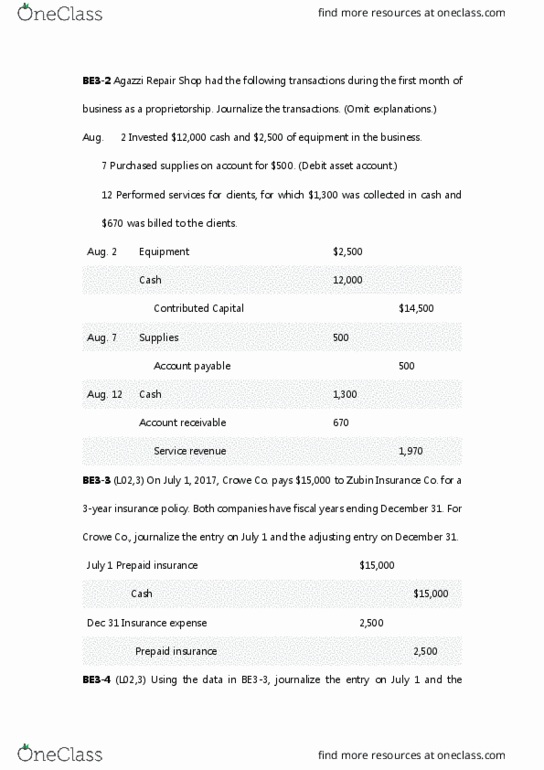

| Wallyâs Widget Company (WWC) incorporated near the end of 2011. Operations began in January of 2012. WWC prepares adjusting entries and financial statements at the end of each month. Balances in the accounts at the end of January are as follows: |

| Cash | $ | 21,620 | Unearned Revenue (30 units) | $ | 5,350 | ||

| Accounts Receivable | $ | 12,650 | Accounts Payable (Jan Rent) | $ | 3,300 | ||

| Allowance for Doubtful Accounts | $ | (1,900) | Notes Payable | $ | 16,000 | ||

| Inventory (35 units) | $ | 2,800 | Contributed Capital | $ | 7,000 | ||

| Retained Earnings â Feb 1, 2012 | $ | 3,520 | |||||

| ⢠| WWC establishes a policy that it will sell inventory at $180 per unit. |

| ⢠| In January, WWC received a $5,350 advance for 30 units, as reflected in Unearned Revenue. |

| ⢠| WWCâs February 1 inventory balance consisted of 35 units at a total cost of $2,800. |

| ⢠| WWCâs note payable accrues interest at a 12% annual rate. |

| ⢠| WWC will use the FIFO inventory method and record COGS on a perpetual basis. |

| February Transactions | |

| 02/01 | Included in WWCâs February 1 Accounts Receivable balance is a $1,400 account due from Kit Kat, a WWC customer. Kit Kat is having cash flow problems and cannot pay its balance at this time. WWC arranges with Kit Kat to convert the $1,400 balance to a note, and Kit Kat signs a 6-month note, at 12% annual interest. The principal and all interest will be due and payable to WWC on August 1, 2012. |

| 02/02 | WWC paid a $650 insurance premium covering the month of February. The amount paid is recorded directly as an expense. |

| 02/05 | An additional 180 units of inventory are purchased on account by WWC for $13,500 â terms 2/15, n30. |

| 02/05 | WWC paid Federal Express $360 to have the 180 units of inventory delivered overnight. Delivery occurred on 02/06. |

| 02/10 | Sales of 150 units of inventory occurred during the period of 02/07 â 02/10. The sales terms are 2/10, net 30. |

| 02/15 | The 30 units that were paid for in advance and recorded in January are delivered to the customer. |

| 02/15 | 25 units of the inventory that had been sold on 2/10 are returned to WWC. The units are not damaged and can be resold. Therefore, they are returned to inventory. Assume the units returned are from the 2/05 purchase. |

| 02/16 | WWC pays the first 2 weeks wages to the employees. The total paid is $2,800. |

| 02/17 | Paid in full the amount owed for the 2/05 purchase of inventory. WWC records purchase discounts in the current period rather than as a reduction of inventory costs. |

| 02/18 | Wrote off a customerâs account in the amount of $2,000. |

| 02/19 | $6,600 of rent for January and February was paid. Because all of the rent will soon expire, the February portion of the payment is charged directly to expense. |

| 02/19 | Collected $10,000 of customersâ Accounts Receivable. Of the $10,000, the discount was taken by customers on $8,000 of account balances; therefore WWC received less than $10,000. |

| 02/26 | WWC recovered $600 cash from the customer whose account had previously been written off (see 02/18). |

| 02/27 | A $950 utility bill for February arrived. It is due on March 15 and will be paid then. |

| 02/28 | WWC declared and paid a $950 cash dividend. |

| Adjusting Entries: |

| 02/29 | Record the $2,800 employee salary that is owed but will be paid March 1. | ||

| 02/29 | WWC decides to use the aging method to estimate uncollectible accounts. WWC determines 8% of the ending balance is the appropriate end of February estimate of uncollectible accounts. | ||

| 02/29 | Record February interest expense accrued on the note payable. | ||

| 02/29 | Record one monthâs interest earned Kit Katâs note (see 02/01).

|

Billâs Lawn Care Mini Practice Part 4

In June, Bill commented to you that he could never figure outhis bank statement, âit never matches the

balance in my accounting recordsâ he tells you. So you explainthat a bank reconciliation is a tool used

to balance the bank statement to the accounting books. He givesyou his bank statement for June, 2014

(shown below). The general ledger shows a balance for theaccount cash of $14,319.00 on June 30,

2014 (detail transactions below). Billâs business only has onechecking account and no other cash

accounts.

Bill has begun to have problems collecting some of his creditaccounts and is considering writing off a

couple of customer account balances. He asks you how these baddebts should be recorded and has

asked you to begin recording bad debt using the allowance methodfor June, 2014. Selected account

balances at the end of June, 2014 are:

Sales $7,200

Sales on Credit $2,900

Accounts Receivable $3,200

As a result of increased focus on collecting accountsreceivable, Bill has decided to extend credit for one

customer, Alan Jones, who owes Billâs Lawn Care $500. Bill andAlan have agreed to a 90-day 6% note

for $500 issued on June 5, 2014.

Instructions:

1. Using the bank statement and the general ledger, prepare abank reconciliation for Billâs Lawn

Care as of June 30, 2014. Record the necessary journal entriesto adjust the books for the

appropriate reconciling items. Start with Page 6 for the journalentries. Explanations are

optional.

2. Using the information given above, calculate the amount ofbad debt using:

Using the chart of accounts, record the journal entry for baddebt expense for Billâs Lawn Care

using the percentage of sales on credit method.

3. Using the note receivable information above and the chart ofaccounts, record the following

entries in the general journal (continue these entries on Page6):

a. Percentage of Sales on Credit = 1.5%

b. Percentage of Accounts Receivable = 1%

a. Receipt of the note in payment of the accounts receivablebalance.

b. Adjusting entry at the end of June, 2014 for the notereceivable. (Round interest

calculations to two decimals)

c. Assume that Alan pays the note and interest in full on thedue date, record the necessary

journal entry. Assume that interest has been accrued at the endof each month.

d. Assume that Alan defaults on the note and interest on the duedate, record the necessary

journal entry. Assume that interest has been accrued at the endof each month.

CHECKING ACCOUNT DETAIL:

DATE | TRANSACTION TYPE & NUMBER | AMOUNT | BALANCE |

BEGINNING BALANCE | $12,850.00 | ||

6/2/2014 | CHECK #1570 | 226.00 | 12,624.00 |

6/5/2014 | CHECK #1571 | 83.00 | 12,541.00 |

6/6/2014 | EFT #43 | 127.00 | 12,414.00 |

6/10/2014 | DEPOSIT #104 | 1,550.00 | 13,964.00 |

6/15/2014 | CHECK #1572 | 145.00 | 13,819.00 |

6/15/2014 | CHECK #1573 | 185.00 | 13,634.00 |

6/20/2014 | DEPOSIT #105 | 885.00 | 14,519.00 |

6/24/2014 | EFT #44 | 143.00 | 14,376.00 |

6/28/2014 | CHECK #1574 | 87.00 | 14,289.00 |

6/28/2014 | CHECK #1575 | 95.00 | 14,194.00 |

6/30/2014 | DEPOSIT #106 | 425.00 | 14,619.00 |

6/30/2014 | CHECK #1576 | 155.00 | 14,464.00 |

6/30/2014 | CHECK #1577 | 145.00 | $14,319.00 |

BANK STATEMENT:

FIRST NATIONAL BANK | ||

ACCOUNT SUMMARY JUNE 30, 2014 | ||

BEGINNING BALANCE | $12,850.00 | |

PAYMENTS | $1,021.00 | |

DEPOSITS | 2,440.00 | |

FEES | 20.00 | |

ENDING BALANCE | $14,249.00 | |

PAYMENTS | ||

DATE | REFERENCE | AMOUNT |

6/5/2014 | 1570 | $266.00 |

6/9/2014 | 1571 | 83.00 |

6/10/2014 | 43 | 127.00 |

6/19/2014 | 1572 | 145.00 |

6/28/2014 | 1573 | 185.00 |

6/28/2014 | NSF | 120.00 |

6/30/2014 | 1575 | 95.00 |

TOTAL PAYMENTS | $1,021.00 | |

DEPOSITS | ||

DATE | REFERENCE | AMOUNT |

6/11/2014 | 104 | $1,550.00 |

6/23/2014 | 105 | 885.00 |

6/30/2014 | INTEREST | 5.00 |

TOTAL DEPOSITS | $2,440.00 | |

FEES | ||

6/30/2014 | SVC CHG | $20.00 |

TOTAL FEES | $20.00 |

Additional Information: Check #1570 waswritten for $266.00, but was recorded incorrectlyin the general ledger. The check was for fuel.

Billâs Lawn Care

Chart of Accounts

Classification | Account Number | Account Name |

ASSETS | 101 | Cash |

110 | Accounts Receivable | |

112 | Allowance for Doubtful Accounts | |

115 | Notes Receivable | |

116 | Interest Receivable | |

120 | Supplies | |

130 | Prepaid Insurance | |

140 | Inventory | |

150 | Equipment | |

155 | Accumulated Depreciation â Equipment | |

LIABILITIES | 201 | Accounts Payable |

220 | Notes Payable | |

225 | Interest Payable | |

OWNERâS EQUITY | 301 | Ownerâs Capital |

305 | Ownerâs Drawings | |

310 | Income Summary | |

REVENUES | 401 | Lawn Service Revenue |

410 | Sales Revenue | |

415 | Sales Returns and Allowances | |

420 | Interest Income | |

COST OF GOODS SOLD | 501 | Purchases |

505 | Purchase Returns and Allowances | |

EXPENSES | 620 | Supplies Expense |

630 | Fuel Expense | |

640 | Repair and Maintenance Expense | |

650 | Advertising Expense | |

660 | Insurance Expense | |

670 | Depreciation Expense | |

680 | Interest Expense | |

690 | Bad Debt Expense | |

695 | Miscellaneous Expense |

Please answer for the following

Bank reconciliation

| Cash balanceper bank statement | ||||

| Adjusted cashbalance per bank | ||||

| Cash balanceper books | ||||

| Adjusted cashbalance per books | ||||

General Ledger

| GENERALJOURNAL | Page | |||

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT |

Bad Debt Calculations

| Term ofNote |

| TotalInterest on Note |

| AccruedInterest June 30, 2014 |

Notes Receivable Calculation

| Percentage ofSales on Credit | |||

| Percentage ofAccounts Receivable | |||

Expert Answer