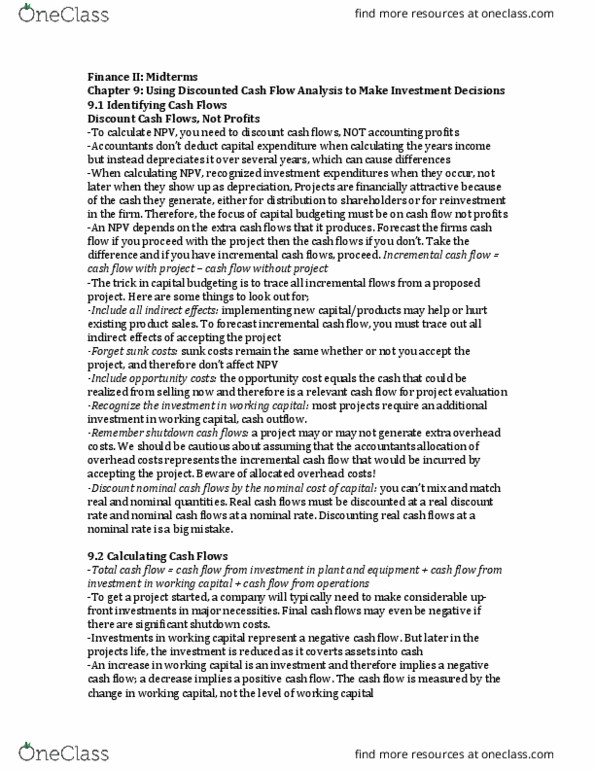

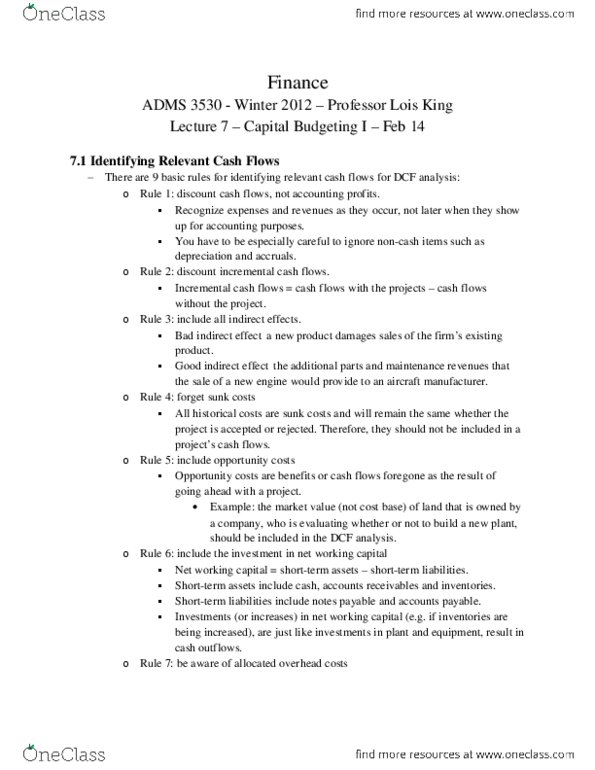

ADMS 3530 Lecture Notes - Operating Cash Flow, Tax Shield, Cash Flow

36 views6 pages

8 May 2012

School

Department

Course

Professor

Get access

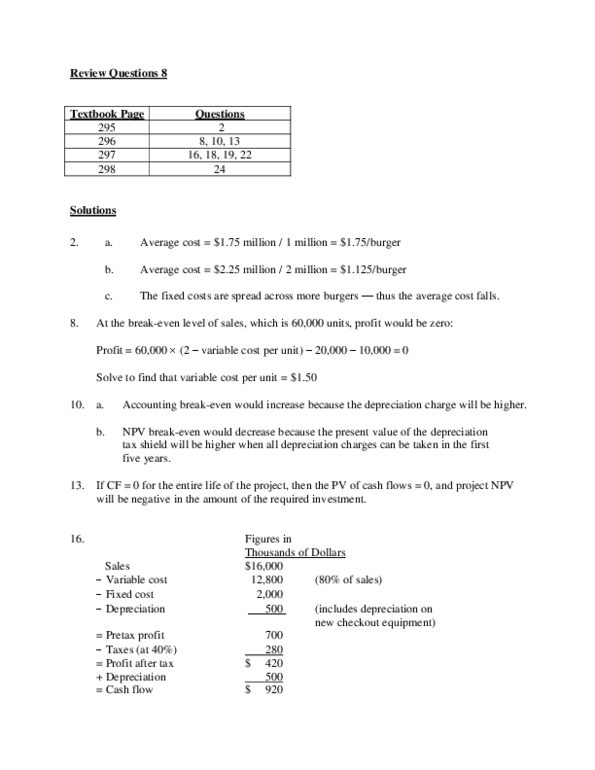

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

The income statement and a schedule reconciling cash flows from operating activities to net income are provided below for Macrosoft Corporation.

| MACROSOFT CORPORATION Income Statement For the Year Ended December 31, 2016 ($ in millions) |

| Revenues and gains: | ||||||

| Sales | $ | 324.00 | ||||

| Gain on sale of cash equivalents | 2.70 | |||||

| Gain on sale of investments | 24.70 | $ | 351.40 | |||

| Expenses and loss: | ||||||

| Cost of goods sold | $ | 127.00 | ||||

| Salaries | 40.70 | |||||

| Interest expense | 12.70 | |||||

| Insurance | 20.70 | |||||

| Depreciation | 10.70 | |||||

| Patent amortization | 4.70 | |||||

| Loss on sale of land | 6.70 | 223.20 | ||||

| Income before tax | 128.20 | |||||

| Income tax expense | 64.10 | |||||

| Net income | $ | 64.10 | ||||

| Reconciliation of Net Income to Net Cash Flows from Operating Activities ($ in millions) | |||

| Net income | $ | 64.10 | |

| Adjustments for noncash effects: | |||

| Depreciation expense | 10.70 | ||

| Patent amortization expense | 4.70 | ||

| Loss on sale of land | 6.70 | ||

| Gain on sale of investment | (24.70 | ) | |

| Decrease in accounts receivable | 6.70 | ||

| Increase in inventory | (12.70 | ) | |

| Increase in accounts payable | 18.70 | ||

| Decrease in bond discount | 1.70 | ||

| Increase in salaries payable | 6.70 | ||

| Decrease in prepaid insurance | 4.70 | ||

| Increase in income tax payable | 10.70 | ||

| Net cash flows from operating activities | $ | 98.00 | |

| Required: |

| Prepare the cash flows from operating activities section of the statement of cash flows (direct method). (Enter your answers in millions rounded to 2 decimal places (i.e., 5,500,000 should be entered as 5.50). Amounts to be deducted should be indicated with a minus sign.) |