ADMS 3595 Lecture Notes - Interest Bearing Note, Accounts Payable, Current Liability

26 May 2013

School

Department

Course

Professor

Document Summary

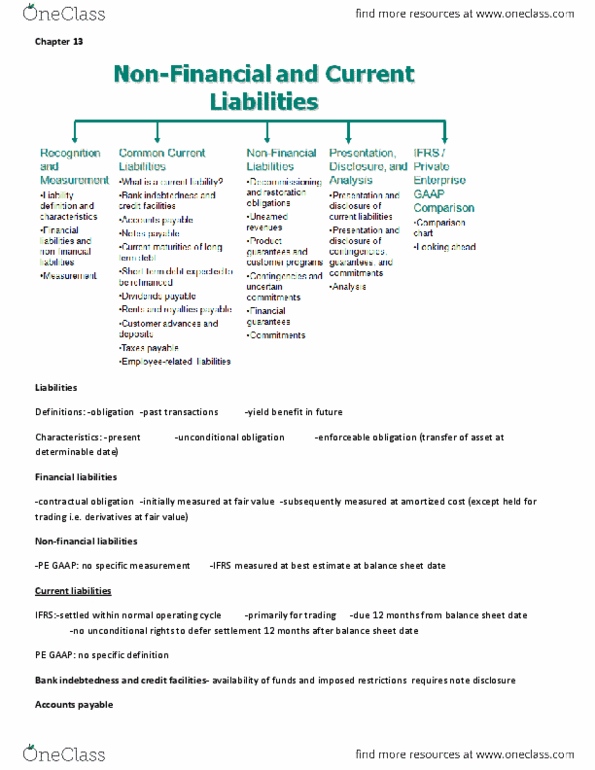

Current definition: a liability is an obligation that arises from past transactions or events, which may result in a transfer of assets. Liabilites have three essential charteristics: they embody a duty or responsibility, the entity has little or no discretion to avoid the duty, the transaction or event that obliges the entity has occured. Proposed definition: a liability of an entity of a present economic obligation for which the entity is the obligor. Financial laibilities: are recongized initially at their fair value but after acquistion most financial liabilites are measured at acqusition cost (except those that are held for trading, suchas derivatives where fair value is used) Financial liabilites is any liability that is a contractual obligation (contact) to either: deliever cash or other financial asset to another party, or, to exchange financial instruments with another party under conditions that are potentially unfavourable. Non financial liabilites: are not payable in cash and the are measured in a different way.