ADMS 1010 Lecture Notes - Lecture 6: Good Governance, Information Asymmetry, Double Taxation

1 Mar 2018

School

Department

Course

Professor

Document Summary

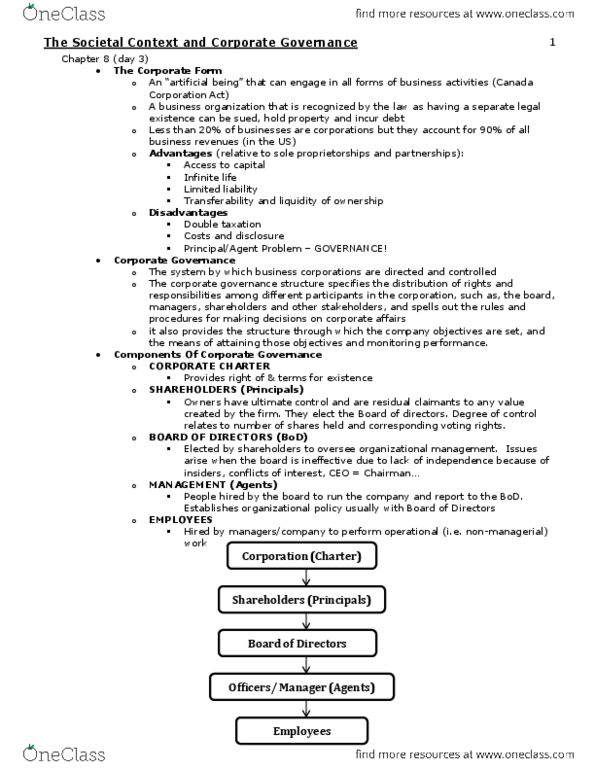

Corporate form; (cid:862)artifi(cid:272)ial (cid:271)ei(cid:374)g(cid:863) that (cid:272)a(cid:374) e(cid:374)gage i(cid:374) all for(cid:373)s of (cid:271)usi(cid:374)ess a(cid:272)tivities. Business organization that is recognized by law as having a separate legal existence and can be sued, hold property & incur debt. Less than 20% are corporations, but only account for 90% of all business revenue. Infinite life (can continue even after the head dies) Limited liability (not responsible to everything, business has own obligation) System in which business corps are directed and controlled. Ensures that managers are acting in the interest of shareholders instead of their own personal interests. Separation of ownership & control in modern corporations. Information asymmetry= owners knowing less about business operations than managers. Managerial incentives & information asymmetry (e. g. managers doing things in the business for their own interests not for the interests of shareholders: solutions: Aligning incentives (providing top managements teams with stock options, shares, (cid:271)o(cid:374)uses, li(cid:374)ki(cid:374)g their pay to the (cid:272)orporatio(cid:374)"s perfor(cid:373)ance)