ADMS 3520 Lecture Notes - Lecture 6: Accountant, Dispositio, Dividend Tax

25 Jun 2018

School

Department

Course

Professor

1 Lecture 6: Non-Arm’s Length Transactions, Departure from Canada and Death of a

Taxpayer

1.1 Recommended Exercises and Self-study Problems

§exercises 9-8, 9-9, 9-10, 8-15, 8-16, 9-14, 9-15, 9-16, 9-17, 11-10

▪self-study problems 9-8, 9-9

▪self-study problems 9-10, 9-11 (ignore the part about farm land)

2 Non-Arm's Length Transfers [CTP 9-142 to 9-172]

▪The non-arm’s length transaction rules determine the deemed proceeds of disposition and

adjusted

cost base (ACB) for gifts and transfers to non-arm's length persons. This is relevant

for

determining: (a) the capital gain at the time of the transfer and (b) the future capital gain

to the

new owner of the property (when he/she sells the property)

▪Rules apply to transfers (gifts or sales) when the transfer is between persons (individuals,

corporations, etc.) who are not at “arm’s length”

▪see example at 9-168 for a theoretical tax avoidance opportunity in non-arm’s length

transfers

▪ITA 251(1): Related persons are deemed to not deal with each other at arm's length

▪It is a question of fact whether others deal at arm's length

▪Related = connected by blood, marriage, common-law partnership or adoption

▪Connected by blood

§= child, parent, grandparent (and great-grandparent, great-great grandparent, etc.)

§

= brother, sister

§= horizontal or vertical relationship on family tree

▪But not aunts, uncles, nieces, nephews, cousins

▪Related by marriage

§

= spouse and in-laws

▪e.g. mother-in-law, daughter-in-law, sister (or brother)-in-law

2.1 Inadequate Consideration [ITA 69]

▪All gifts are deemed dispositions at FMV (even gifts to arm’s length persons) except for gifts

to

spouses [ITA 69 and 73(1)]

▪See Figure 9-2

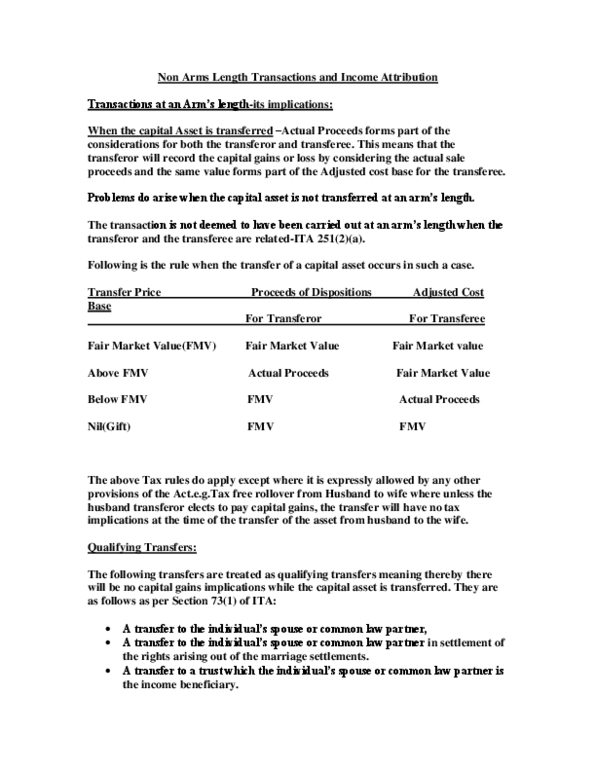

2.2 Sales to non-arm's length persons

▪Sales to non-arm’s length persons should take place at FMV except for transfers to spouses

because the one-sided adjustment in ITA 69 is intentionally harsh

▪If the sales price is > FMV, the purchaser's ACB is deemed to be FMV

▪If the sales price is < FMV, the seller's proceeds of disposition is deemed to be FMV

▪Sales price too low (< FMV) is the more common situation

find more resources at oneclass.com

find more resources at oneclass.com

find more resources at oneclass.com

find more resources at oneclass.com

▪read 9-154 carefully

▪A gift or sale to a spouse automatically occurs at tax cost (ACB for capital property, UCC for

depreciable property) [ITA 73(1)]

▪However, if the transferor makes an election not to have ITA 73 apply, ITA 69 and the above

rules apply (i.e., the disposition will occur at FMV). These rules for spouses apply to spousal

trusts and common-law partners

2.3 Attribution Rules [9-187 to 9-201]

▪The income attribution rules can determine the tax on the future income and capital gains

earned by the new owner of property. Special rules apply when (a) a property is loaned or

transferred to a spouse or minor child (child under 18) or minor niece or nephew [ITA 74.1

(income) and 74.2 (capital gains)]; (b) a property is loaned to another non-arm’s length

person (e.g., a 30 year old child, an 84 year old parent) and one of the main purposes of the

loan was to reduce the income of the lender [ITA 56(4.1)]

▪The attribution rules move the income (and capital gains in the case of a spouse) from the

family member’s tax return to the lender/transferor’s tax return

▪If a loan or transfer is to a spouse, any income or capital gains earned by the spouse is

taxed in the lender/transferor's hands [ITA 74.1 (1) and 74.2(1)]

▪If a loan or transfer is to a minor child (or minor niece or nephew), only the income

earned by the minor (not capital gains) is taxed in the lender/transferor's hands [ITA

74.1(2)]

2.4 Tax on Split Income [the Kiddie Tax] [11-110 to 11-120]

▪The tax on split income (referred to as the kiddie tax) applies to certain types of income

earned by minors, including dividends from private corporations (i.e., incorporated small

businesses) [ITA 120.4]

▪Because it is a tax at the very top marginal tax rate, it essentially eliminates income splitting

benefits from children being shareholders in private corporations (until they are 18 years old

or older)

▪The kiddie tax also applies when children earn business income (typically earned through a

trust or partnership) that is from the business of a related individual

▪The kiddie tax is not really an “attribution” rule because it does not move the income; it

simply taxes it at the top rate

▪As per the June

6,

2011

Federal

Budget,

for certain capital gains realized after March

22, 2011, if a minor has a capital gain on the non-arm’s

length

disposition

of shares

that would have been subject to the kiddie tax (if dividends were paid) then the

capital gain will be deemed to be a dividend . Hence the capital gain will:

•be subject to the kiddie tax;

•will not be eligible for capital gains inclusion rates;

and

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lecture 6: non-arm"s length transactions, departure from canada and death of a. Recommended exercises and self-study problems exercises 9-8, 9-9, 9-10, 8-15, 8-16, 9-14, 9-15, 9-16, 9-17, 11-10 self-study problems 9-8, 9-9 self-study problems 9-10, 9-11 (ignore the part about farm land) The non-arm"s length transaction rules determine the deemed proceeds of disposition and adjusted cost base (acb) for gifts and transfers to non-arm"s length persons. This is relevant for determining: (a) the capital gain at the time of the transfer and (b) the future capital gain to the new owner of the property (when he/she sells the property) Rules apply to transfers (gifts or sales) when the transfer is between persons (individuals, corporations, etc. ) who are not at arm"s length see example at 9-168 for a theoretical tax avoidance opportunity in non-arm"s length transfers. Ita 251(1): related persons are deemed to not deal with each other at arm"s length.