ECON 4400 Lecture Notes - Capital Cost Allowance, Income Tax

Document Summary

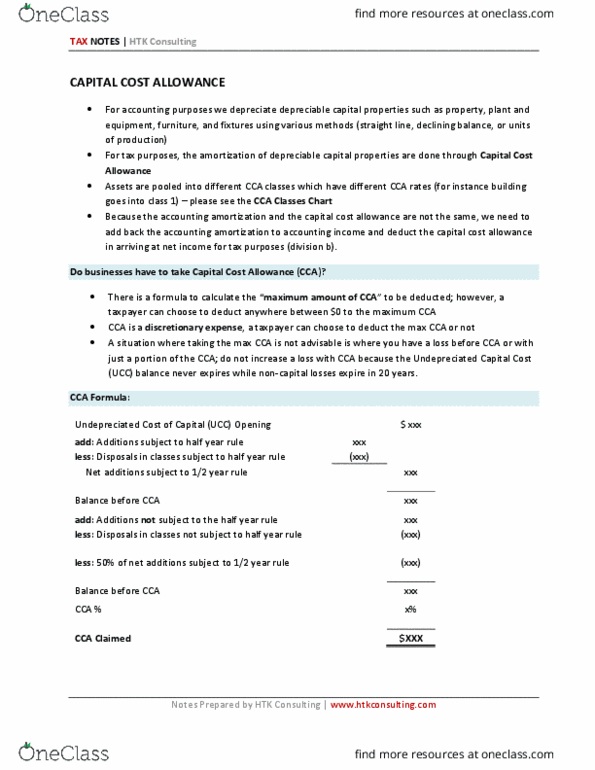

The amount calculated is the maximum cca. It does not need to be deducted if taxpayer does not want to deduct it. Capital cost allowance: year rule, recaptured cca, terminal loss, prorate cca for short years, capital gain if asset sold for more than original cost. In year of purchase, of regular cca is deducted. Year adjustment is made in column 7 of cca schedule. (additions disposals) (use nil if amount is negative) When an asset is sold for an amount less than its undepreciated capital cost, and all the assets of the class are disposed of. A terminal loss is fully deductible in year of disposal. The difference between the proceeds and ucc is the amount of the terminal loss. When an asset is sold for an amount greater than the. The difference between the proceeds and the ucc is taxable income called recaptured cca . It is not necessary to sell all assets in the class.