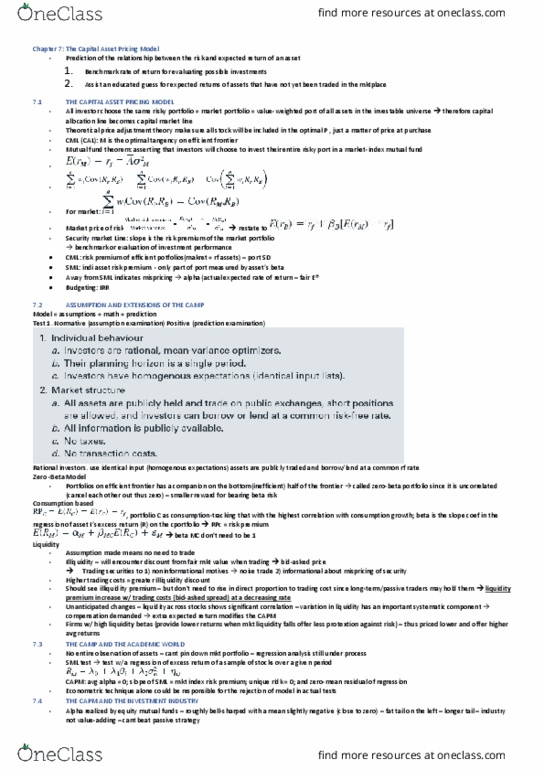

FINE 3200 Lecture Notes - Lecture 5: Modern Portfolio Theory, Risk Premium, Irving Fisher

Document Summary

Speculation: considerable business risk (risk sufficient to affect the decision) in obtaining commensurate gain (positive expected profit beyond the risk-free alternative = risk premium) risk-premium trade-off. Ga(cid:373)(cid:271)le la(cid:272)k of (cid:862)(cid:272)o(cid:373)(cid:373)e(cid:374)surate gai(cid:374)(cid:863) enjoyment of risk only. Heterogeneous expectations: same scenario but people will assign different probabilities for each outcome. Fair game: zero-risk premium risk-averse investor rejects fair game or worse. Risk-averse only risk-free or speculative prospects w/ positive risk premiums penalize the expected rate of return of a risky portfolio by a certain percentage to account for risk involved. Utility: scored assigne to port based on expected return and risk. Utility value: higher expected return + lower risk = more attractive severely the primary goal is to max return. , a = i(cid:374)de(cid:454) of i(cid:374)(cid:448)estor"s a(cid:448)ersio(cid:374) more risk aversion penalizes risky investments more. Certainty equivalent rate: rate risk-free investment would need to offer w/ certainty to be considered equally attractive to a risky portfolio.