ACC 2203 Lecture Notes - Lecture 2: Finished Good, Deutsche Luft Hansa, Sigma Corporation

2 Jun 2018

School

Department

Course

Professor

CHAPTER 2 – JOB COSTING

!

!

_________________________________________________________________________________________________________________________________

© COPYRIGHTED 2014. Y. PAN. ALL MATERIALS ARE COPYRIGHTED AND MAY NOT BE DUPLICATED, DISTRIBUTED,

TRANSFERRED OR USED WITHOUT PERMISSION. EMAIL: YU.[email protected]

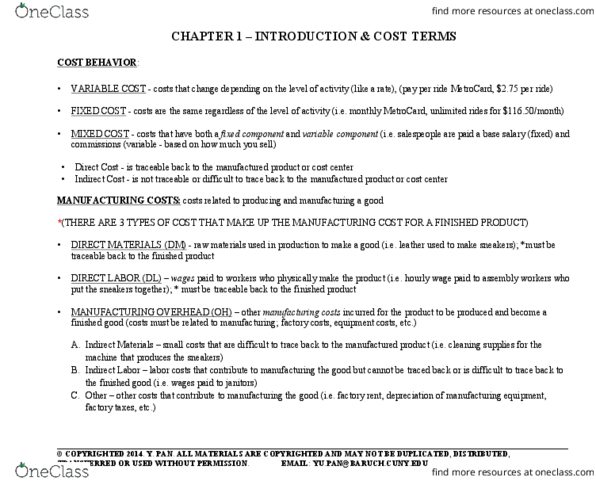

JOB COSTING: Job costing is how we estimate the cost of a product

What makes up the cost of a product?

-Direct costs are easy to trace back to the finished/manufactured product and significant enough to keep track of

-Indirect costs are difficult to trace back to the finished/manufactured product and are not significant enough to keep track of

1. Direct Materials ! traceable back to the manufactured product

2. Direct Labor ! traceable back to the manufactured product

3. Manufacturing Overhead ! uses an allocation base (indirect, difficult to trace the costs back to the product)

MANUFACTURING OVERHEAD:

How do we allocate overhead?

1. Start with the allocation base: It’s almost always given in the problem. (Usually some type of hours, i.e. direct labor hours,

machine hours, etc. However, it can also be a cost too such as direct labor cost ($) so READ THE QUESTION CAREFULLY!)

2. Find the estimated total overhead for the year: This is usually based on the company’s past overhead costs.

3. Solve for the predetermined overhead rate: This is the rate we use to find how much overhead we should apply to a product.

PREDETERMINED OVERHEAD

RATE

=

Estimated Total Overhead ($ amount)

Estimated Allocation Base (usually hours, can be a cost ($) as well)

Estimated Overhead – amount of overhead you expect for the year; usually based on the company’s past performance

*Applied Overhead – amount of overhead you applied or allocated to a product, useful for forecasting the product’s cost

Actual Overhead – amount of overhead cost you incur at the end of the manufacturing process/period, you won’t know until the end

CHAPTER 2 – JOB COSTING

!

!

_________________________________________________________________________________________________________________________________

© COPYRIGHTED 2014. Y. PAN. ALL MATERIALS ARE COPYRIGHTED AND MAY NOT BE DUPLICATED, DISTRIBUTED,

TRANSFERRED OR USED WITHOUT PERMISSION. EMAIL: YU.[email protected]

APPLIED OVERHEAD

=

PREDETERMINED OVERHEAD

RATE

X

ACTUAL ALLOCATION BASE

APPLIED OVERHEAD

=

Estimated Total Overhead ($ amount)

X

ACTUAL ALLOCATION BASE

Estimated Allocation Base (usually

hours)

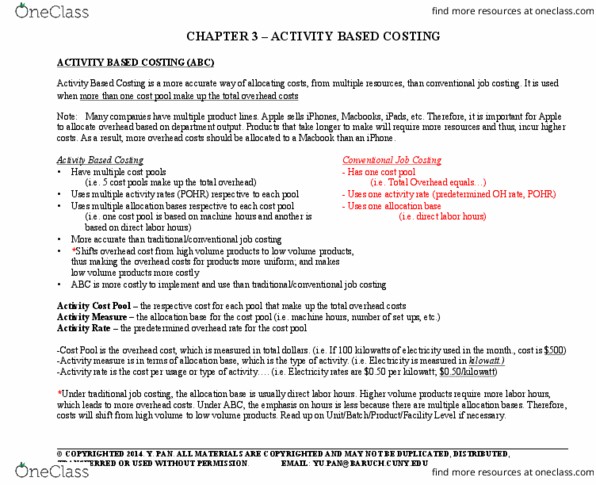

To help understand the concept of applying overhead, consider the following:

Machines and equipment used to manufacture products are included in the product’s cost (part of overhead). However, the

same machine can be used to manufacture different products (phones, tablets, and computers). Therefore “part of the cost of the

machine’s total expense” will need to be allocated to each product. Overhead will be allocated or applied based on the machine usage

to make each product. A computer will take longer to make than a phone. Therefore, more overhead cost will be applied to a computer

than a phone.

CHAPTER 2 – JOB COSTING

!

!

_________________________________________________________________________________________________________________________________

© COPYRIGHTED 2014. Y. PAN. ALL MATERIALS ARE COPYRIGHTED AND MAY NOT BE DUPLICATED, DISTRIBUTED,

TRANSFERRED OR USED WITHOUT PERMISSION. EMAIL: YU.[email protected]

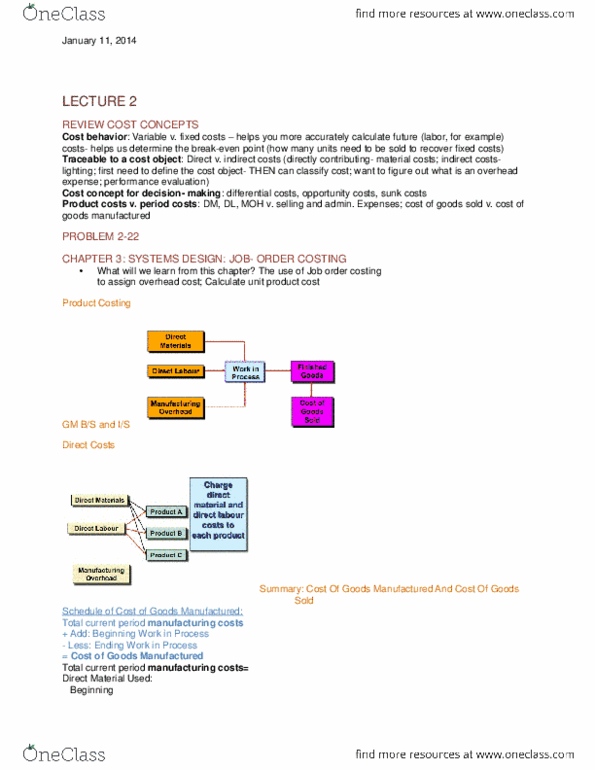

Direct Materials

--->

Actual cost traceable back to the product

Direct Labor

--->

Actual cost traceable back to the product

Manufacturing Overhead

--->

Applied cost based on the predetermined overhead rate and the actual allocation base

Job Costing -Work In Process

Beginning WIP

+

Direct Material

+

Direct Labor

+

*Applied MOH

- Cost of Goods Manufactured

=

Ending WIP

Manufacturing cost (or product cost) = DM + DL + Applied MOH

If given Ending WIP and not COGM, rewrite to solve for COGM

COGM = Beg WIP + DM + DL + Applied MOH - Ending WIP

*Always use applied overhead during job costing NOT estimated or actual overhead. If only one overhead is given then use that to

solve the problem.

Document Summary

Job costing: job costing is how we estimate the cost of a product. Direct costs are easy to trace back to the finished/manufactured product and significant enough to keep track of. How do we allocate overhead: start with the allocation base: it"s almost always given in the problem. (usually some type of hours, i. e. direct labor hours, machine hours, etc. Estimated allocation base (usually hours, can be a cost ($) as well) Estimated overhead amount of overhead you expect for the year; usually based on the company"s past performance. *applied overhead amount of overhead you applied or allocated to a product, useful for forecasting the product"s cost. Actual overhead amount of overhead cost you incur at the end of the manufacturing process/period, you won"t know until the end. To help understand the concept of applying overhead, consider the following: Machines and equipment used to manufacture products are included in the product"s cost (part of overhead).