ECON 160 Lecture Notes - Lecture 34: Marginal Cost, Economic Equilibrium, Sunk Costs

Get access

Related Documents

Related Questions

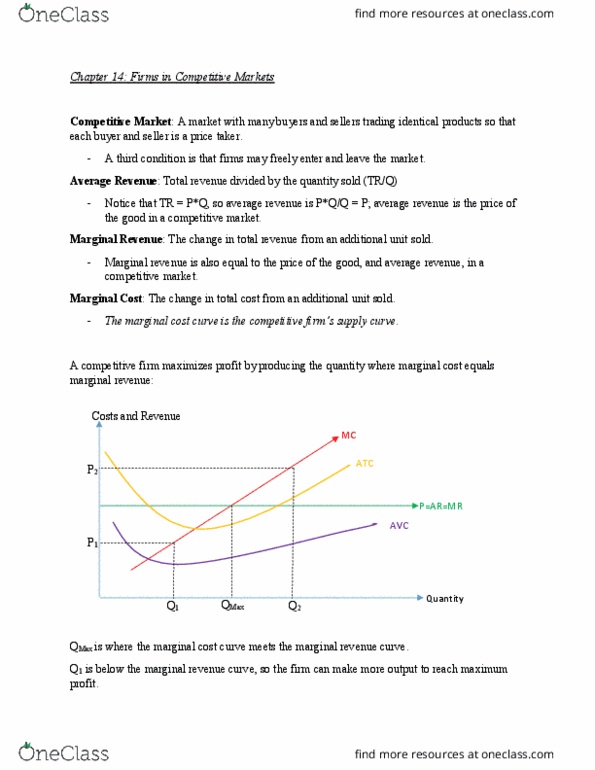

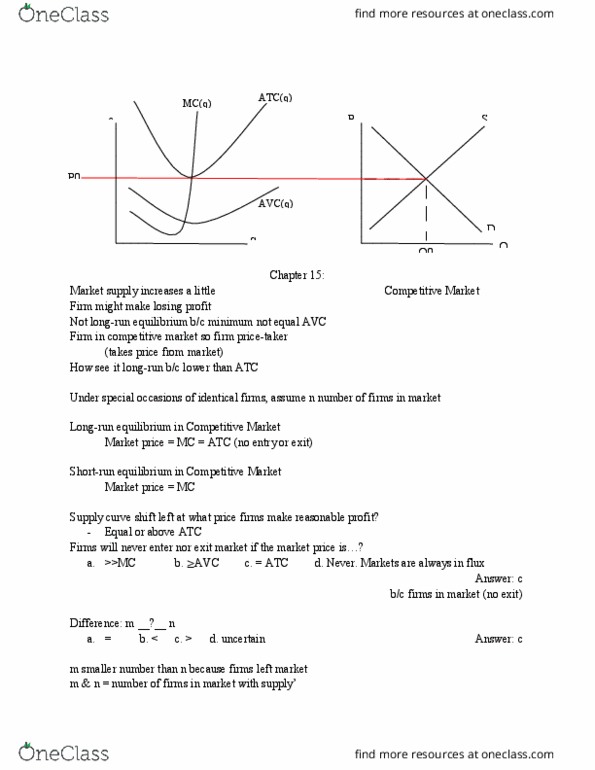

Deriving the short-run supply curve.

Consider the competitive market for halogen lamps. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. For each price in the following table, use the graph to determine the number of lamps this firm would produce in order to maximize its profit. Assume that when the price is exactly equal to the average variable cost, the firm is indifferent between producing zero lamps and the profit-maximizing quantity. Also, indicate whether the firm will produce, shut down, or be indifferent between the two in the short run. Lastly, determine whether it will make a profit, suffer a loss, or break even at each price.

|

Price (dollars per lamp) |

|

Produce or shutdown

|

Profit or loss

|

|

15 |

|

|

|

|

20 |

|

|

|

|

25 |

|

|

|

|

55 |

|

|

|

|

70 |

|

|

|

|

85 |

|

|

|