ACCT-2010 Lecture 2: Chapter 2 - The Balance Sheet

33 views2 pages

29 Jan 2017

School

Department

Course

Professor

Document Summary

Cash +20,000: loan, equipment equipment +9,600, pay supplier, order software, receive software, receive. Assets resources controlled by a company that have a measurable value that benefits the company by increase cash inflows and reducing cash outflows. Liabilities measurable amount that company owes to creditors. Stockholders" equity owners" claim to resources owned by company. Companies have two sources of financing: debt financing = liabilities, equity financing = stockholders" equity. Key features of financing and investing activities within a company: companies document their activities, company receives something and gives something, each exchange has a dollar amount determined for it. External exchanges involves assets, liabilities, and stockholders" equity between the company and someone else. Internal events events within a company, ex: uses assets to make a product. Accounting cycle or method: analyze the transaction using 3 steps above (key features of financing and investing , record, summarize. Transaction business activity that affects the accounting equation.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers

Related Documents

Related Questions

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

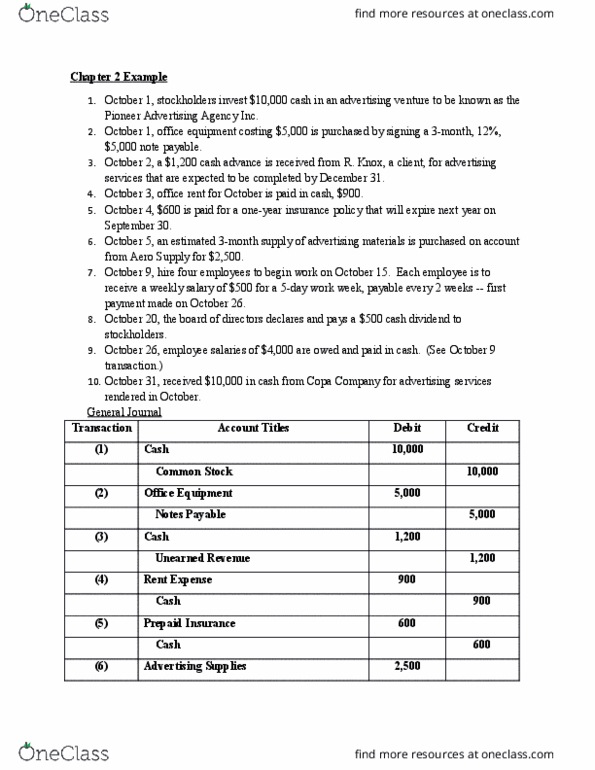

Record journal entries for the summarized transactions for2010 (e.g. items 1 - 10 below)

Susieâs Catering Service, a corporation, began business onJanuary 1, 2009. At the end of Year 1, December 31, 2009, thecompanyâs post-closing trial balance appeared as follows:

| a/c # | Account name | Balance |

| 100 | Cash | 38,500 |

| 105 | Accounts Receivable | 4,000 |

| 110 | Supplies | 2,200 |

| 115 | Prepaid Insurance | 1,800 |

| 160 | Equipment | 15,000 |

| 165 | A/D-Equipment | (3,000) |

| Total Assets | 58,500 | |

| 200 | Accounts Payable | 6,300 |

| 205 | Notes Payable (short-term) | 3,000 |

| 210 | Wages Payable | 1,200 |

| 215 | Interest Payable | 0 |

| 220 | Income Taxes Payable | 700 |

| 225 | Advances from Customers | 2,200 |

| 250 | Notes Payable (long-term) | 9,000 |

| 300 | Contributed Capital | 12,000 |

| 305 | Retained Earnings | 24,000 |

| Total Liabilities & Owners' Equity | 58,500 | |

| 310 | Dividends Declared | 0 |

| 400 | Service Revenue | 0 |

| 505 | Depreciation Expense | 0 |

| 510 | Wages Expense | 0 |

| 515 | Insurance Expense | 0 |

| 520 | Supplies Expense | 0 |

| 600 | Interest Expense | 0 |

| 650 | Income Tax Expense | 0 |

A summary of transactions (1 â 10) which occurred during 2010 areas follows (to be entered into the âgeneral journalâ at December30, 2010):

(1). Earned revenue of $125,000 of which $102,400 had beencollected in cash with $22,600 still due from customers. Thisamount does not include the balance in the âAdvances fromCustomersâ account which will be considered in transaction<8.

(2). Purchased equipment for $2,400 cash.

(3). Issued 1,000 additional shares of stock and received $7,000cash.

(4). Paid cash wages of $56,200, of which $1,200 was payment on thebeginning of the year Wages Payable balance, with the remaining$55,000 paid for work performed during the current year.

(5). Purchased supplies costing $3,000 for future use during theyear. $600 of these purchases remain unpaid for at the end of theyear [i.e. $2,400 was paid in cash with $600 still open on accountto vendors]

(6). Collected the entire Accounts Receivable balance that existedat the beginning of the year.

(7). Paid off all of the beginning Accounts Payable balance.

(8). Near the end of the year received a $1,650 deposit from acustomer for services to be performed next year.

(9). Declared and paid a cash dividend of $9,500.

(10). Paid the âIncome Taxes Payableâ balance that existed at thebeginning of the year.