ACCTG 102 Lecture Notes - Lecture 22: Capital Account

Document Summary

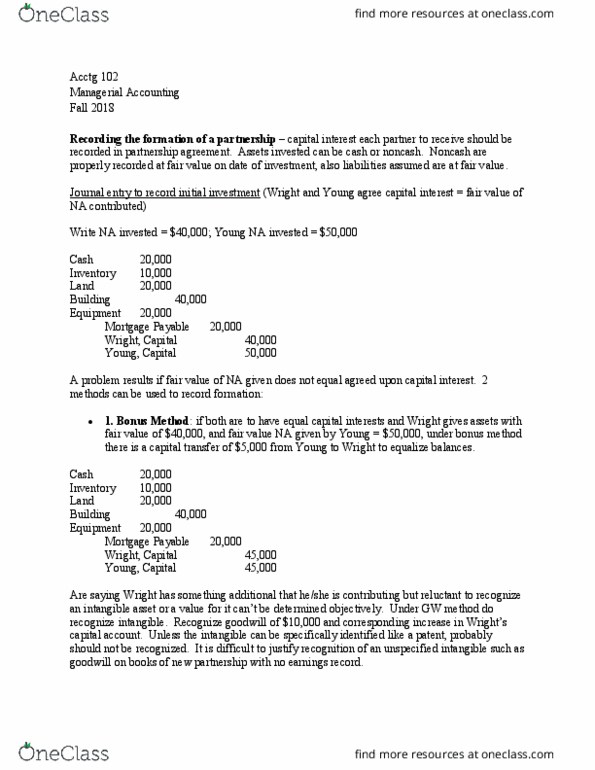

Methods of recording changes in membership of the partnership. Bonus method any difference between the assets invested and the credit to the new partners" capital account is adjusted to the capital accounts of the other partners. With a withdrawal the difference between the recorded value of the assets withdrawn and the debit to withdrawing partner account is adjusted to remaining partners" accounts. Difference between value implied by the amount of consideration negotiated and value on books. Bonus and goodwill method used for either admission of a new partner or the withdrawal of a partner. A partner is entitled to sell his/her interest in firm but other partners are not forced to accept the new member. All partners have to agree to let them manage, otherwise only right to receive profits and assets upon liquidation. If a sold of his interest, the payment goes directly to the partner who sold it.