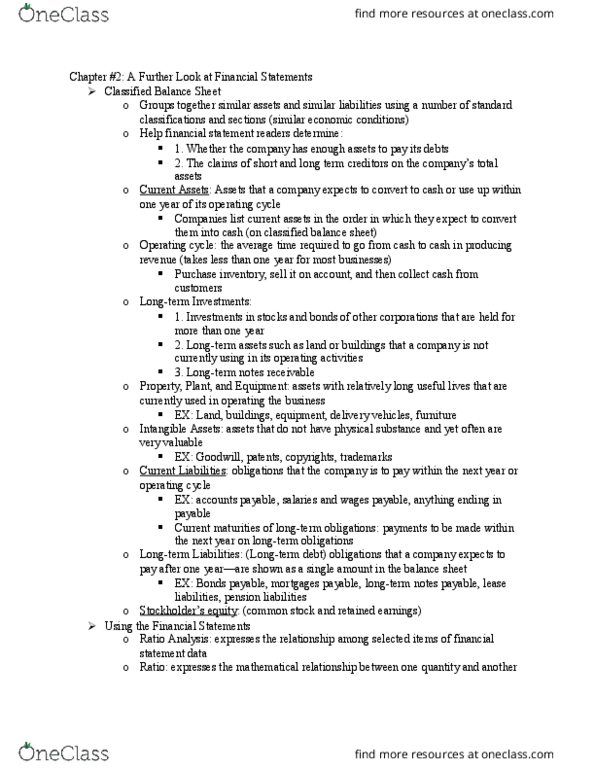

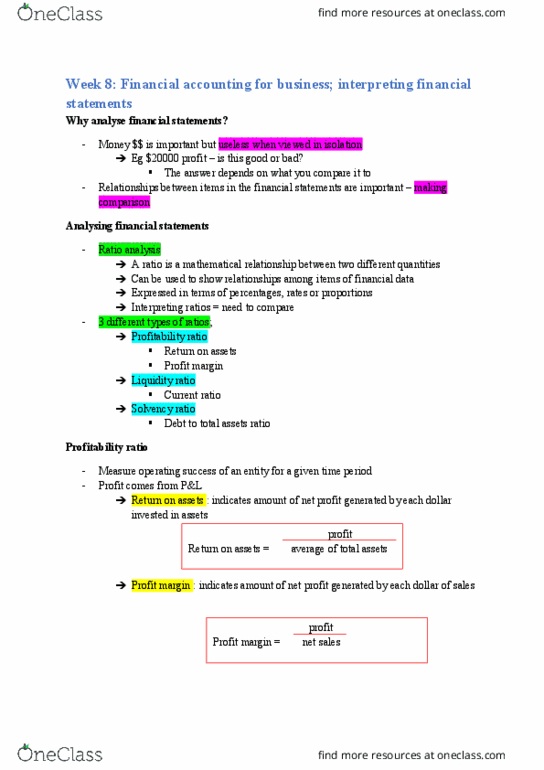

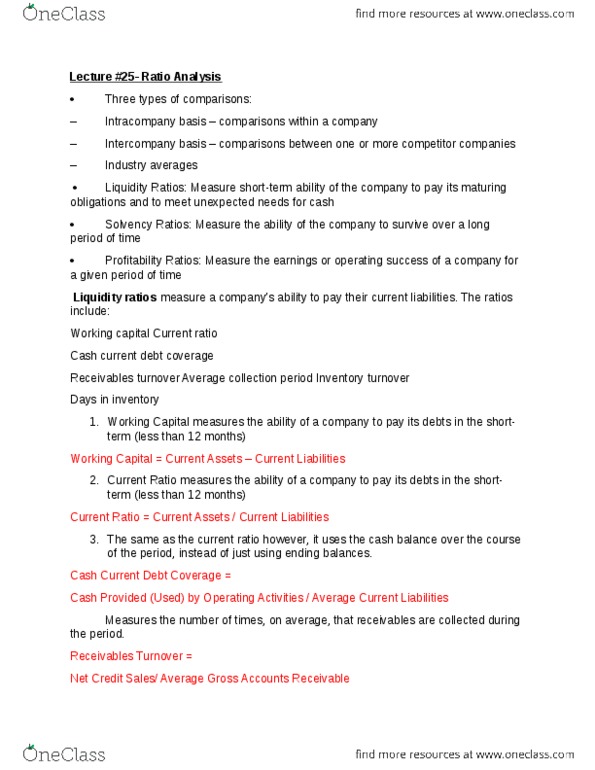

ACCT 101 Lecture Notes - Lecture 2: Cash Flow, Current Liability, Financial Statement

Document Summary

Get access

Related Documents

Related Questions

Chapter 12âFinancial Statement Analysis (10points)

MUMULTIPLECHOICE

1. 1. The relationship of $325,000to $125,000, expressed as a ratio, is

a. | 2.0 to 1 |

b. | 2.6 to 1 |

c. | 2.5 to 1 |

d. | 0.45 to 1 |

2. In a common size income statement,the 100% figure is:

a. | net cost of goods sold. |

b. | net income. |

c. | gross profit. |

d. | net sales. |

3. Based on the following data for thecurrent year, what is the number of days' sales in accountsreceivable?

Net sales on account during year | $584,000 |

Cost of merchandise sold during year | 300,000 |

Accounts receivable, beginning of year | 45,000 |

Accounts receivable, end of year | 35,000 |

Inventory, beginning of year | 90,000 |

Inventory, end of year | 110,000 |

a. | 7.3 |

b. | 2.5 |

c. | 14.6 |

d. | 25 |

4. Based on the following data for thecurrent year, what is the number of days' sales in inventory?

Net sales on account during year | $1,204,500 |

Cost of merchandise sold during year | 657,000 |

Accounts receivable, beginning of year | 75,000 |

Accounts receivable, end of year | 85,000 |

Inventory, beginning of year | 85,600 |

Inventory, end of year | 98,600 |

a. | 51.2 |

b. | 44.4 |

c. | 6.5 |

d. | 7.5 |

5. The number of times interest expenseis earned is computed as

a. | net income plus interest expense, divided by interestexpense |

b. | income before income tax plus interest expense, divided byinterest expense |

c. | net income divided by interest expense |

d. | income before income tax divided by interest expense |

6. The current ratio is

a. | used to evaluate a company's liquidity and short-term debtpaying ability. |

b. | is a solvency measure that indicated the margin of safety of anoteholder or bondholder. |

c. | calculated by dividing current liabilities by currentassets. |

d. | calculated by subtracting current liabilities from currentassets. |

7. A company with $70,000 in current assets and $50,000 incurrent liabilities pays a $1,000 current liability. As a result ofthis transaction, the current ratio and working capital will

a. | both decrease. |

b. | both increase. |

c. | increase and remain the same,respectively. |

d. | remain the same and decrease,respectively. |

8. Hsu Company reported the following onits income statement:

Income before income taxes | $420,000 | |

Income tax expense | 120,000 | |

Net income | $300,000 |

An analysis of the income statement revealed that interestexpense was $80,000. Hsu Company's times interest earned was

a. | 8 times. |

b. | 6.25 times. |

c. | 5.25 times. |

| d. e. | 5 times. None of the above |

9. The following information pertains toBrock Company. Assume that all balance sheet amounts represent bothaverage and ending balance figures. Assume that all sales were oncredit.

Assets

Cash and short-term investments | $ 40,000 | ||

Accounts receivable (net) | 30,000 | ||

Inventory | 25,000 | ||

Property, plant and equipment | 215,000 | ||

Total Assets | $310,000 | ||

Liabilities and Stockholdersâ Equity

Current liabilities | $ 60,000 | ||

Long-term liabilities | 95,000 | ||

Stockholdersâ equity-common | 155,000 | ||

Total Liabilities and stockholdersâ equity | $310,000 | ||

Income Statement

Sales | $ 90,000 | ||

Cost of goods sold | 45,000 | ||

Gross margin | 45,000 | ||

Operating expenses | 20,000 | ||

Net income | $ 25,000 | ||

Number of shares of common stock | 6,000 |

Market price of common stock | $20 |

What is the current ratio for thiscompany?

a. | 1.42 |

b. | 0.78 |

c. | 1.58 |

| d. e | 0.67 None of the above |

11. Basedon the above data, what is the amount of quick assets?

a. | $168,000 |

b. | $96,000 |

c. | $60,000 |

| d. e | $61,000 None of the above |

12. Basedon the above data, what is the amount of working capital?

a. | $213,000 |

b. | $113,000 |

c. | $153,000 |

| d. e | $39,000 None of the above |

13. Thetendency of the rate earned on stockholders' equity to varydisproportionately from the rate earned on total assets issometimes referred to as

a. | leverage |

b. | solvency |

c. | yield |

d. | quick assets |

The balance sheets at the end of each of the first two years ofoperations indicate the following:

2012 | 2011 | |

Total current assets | $600,000 | $560,000 |

Total investments | 60,000 | 40,000 |

Total property, plant, and equipment | 900,000 | 700,000 |

Total current liabilities | 125,000 | 65,000 |

Total long-term liabilities | 350,000 | 250,000 |

Preferred 9% stock, $100 par | 100,000 | 100,000 |

Common stock, $10 par | 600,000 | 600,000 |

Paid-in capital in excess of par-common stock | 75,000 | 75,000 |

Retained earnings | 310,000 | 210,000 |

14. Ifnet income is $115,000 and interest expense is $30,000 for 2012what is the rate earned on total assets for 2012 (round percent toone decimal point)?

a. | 9.3% |

b. | 10.1% |

c. | 8.0% |

| d. e. | 7.4% None of the above |

15. Ifnet income is $115,000 and interest expense is $30,000 for 2012,what is the rate earned on stockholders' equity for 2012 (roundpercent to one decimal point)?

a. | 10.6% |

b. | 11.1% |

c. | 12.4% |

| d. e. | 14.0% None of the above |

16. Ifnet income is $115,000 and interest expense is $30,000 for 2012,what are the earnings per share on common stock for 2012, (round totwo decimal places)?

a. | $2.07 |

b. | $1.92 |

c. | $1.77 |

| d. e. | $1.64 None of the above |

17. Theparticular analytical measures chosen to analyze a company may beinfluenced by all of the following except:

a. | industry type |

b. | capital structure |

c. | diversity of business operations |

d. | product quality or service effectiveness |

18. In2012 Robert Corporation had net income of $250,000 and paiddividends to common stockholders of $50,000. They had 50,000 sharesof common stock outstanding during the entire year. RobertCorporation's common stock is selling for $50 per share on the NewYork Stock Exchange.

Robert Corporation's price-earnings ratio is

a. | 10 times. |

b. | 5 times. |

c. | 2 times. |

| d. e. | 8 times. None of the above |

19. Leveraging implies that a company

a. | contains debt financing. |

b. | contains equity financing. |

c. | has a high current ratio. |

d. | has a high earnings per share. |

20. Percentage analyses, ratios, turnovers, and other measures offinancial position and operating results are

a. | a substitute for sound judgment. |

b. | useful analytical measures. |

c. | enough information for analysis, industry information is notneeded. |

d. | unnecessary for analysis, but reaction is better. |

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

1. Which of thefollowing below generally is the most useful in analyzing companiesof different sizes

a. | comparative statements |

b. | common-sized financialstatements |

c. | price-level accounting |

d. | audit report |

2. What type ofanalysis is indicated by the following?

|

|

| Increase(Decrease*) | |

| 2010 | 2009 | Amount | Percent |

Current assets | $ 380,000 | $ 500,000 | $120,000* | 24%* |

Fixed assets | 1,680,000 | 1,500,000 | 180,000 | 12% |

a. | vertical analysis |

b. | horizontalanalysis |

c. | liquidity analysis |

d. | common-size analysis |

3. Assume thefollowing sales data for a company:

| 2010 | 750,000 |

| 2009 | 500,000 |

What is the percentage increase in sales from 2009 to 2010?

a. | 25% |

b. | 66.7% |

c. | 50% 250,000/500,000 = .5 or 50% |

d. | 150% |

4. In performing avertical analysis, the base for cost of goods sold is

a. | Total selling expenses. |

b. | Net sales. |

c. | Total expenses. |

d. | Total revenues. |

5. The ability of abusiness to pay its debts as they come due and to earn a reasonableamount of income is referred to as

a. | solvency and leverage |

b. | solvency and profitability |

c. | solvency andliquidity |

d. | solvency and equity |

6. Which of thefollowing is not an analysis usedin assessing solvency?

a. | number of times interest charges are earned |

b. | current position analysis |

c. | ratio of net sales toassets |

d. | inventory analysis |

7. A company withworking capital of $500,000 and a current ratio of 2.5 pays a$85,000 short-term liability. The amount of working capitalimmediately after payment is

a. | $585,000 |

b. | $415,000 |

c. | $500,000 |

d. | $85,000 |

8. Based on thefollowing data for the current year, what is the accountsreceivable turnover?

Net sales on account during year | $500,000 |

Cost of merchandise sold during year | 300,000 |

Accounts receivable, beginning of year | 45,000 |

Accounts receivable, end of year | 35,000 |

Inventory, beginning of year | 90,000 |

Inventory, end of year | 110,000 |

a. | 12.5 =$500,000/ 40000 = 12.5 (45,000+35,000)/2 =40,000 |

b. | 11.1 |

c. | 10.0 |

d. | 14.3 |

9. Based on thefollowing data for the current year, what is the inventoryturnover?

Net sales on account during year | $500,000 |

Cost of merchandise sold during year | 330,000 |

Accounts receivable, beginning of year | 45,000 |

Accounts receivable, end of year | 35,000 |

Inventory, beginning of year | 90,000 |

Inventory, end of year | 110,000 |

a. | 3.3 $330,000 /100,000 =3.3 |

b. | 8.3 |

c. | 3.7 |

d. | 3.0

|

10. The primary advantages of theaverage rate of return method are its ease of computation and thefact that:

a. | it is especially useful to managers whose primary concern isliquidity |

b. | there is less possibility of loss from changes in economicconditions and obsolescence when the commitment is short-term |

c. | it emphasizes the amountof income earned over the life of the proposal |

d. | rankings of proposals are necessary |

11. The expected average rate ofreturn for a proposed investment of $800,000 in a fixed asset, witha useful life of four years, straight-line depreciation, noresidual value, and an expected total net income of $240,000 forthe 4 years, is:

a. | 30% |

b. | 15% |

c. | 60% |

d. | 7.5% |