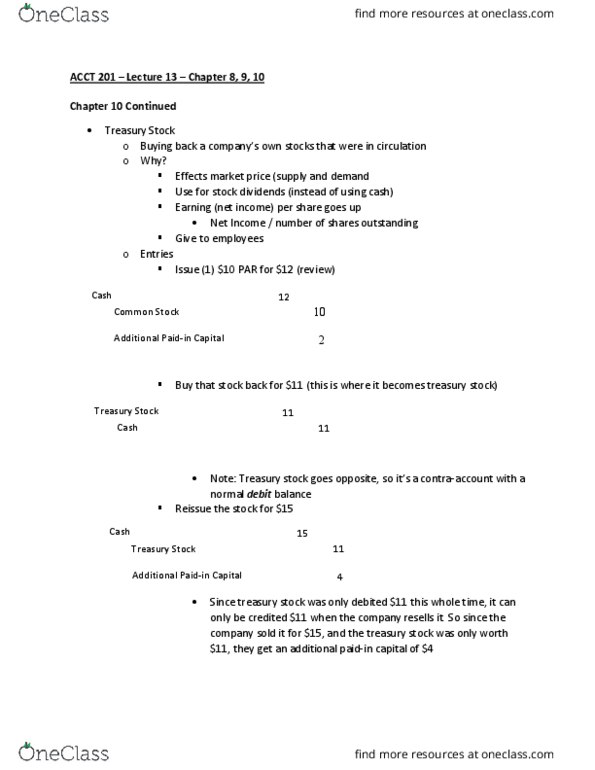

ACCT 201 Lecture Notes - Lecture 10: Treasury Stock, Preferred Stock, Stock Split

ACCT 201 – Lecture 12 – Chapter 10

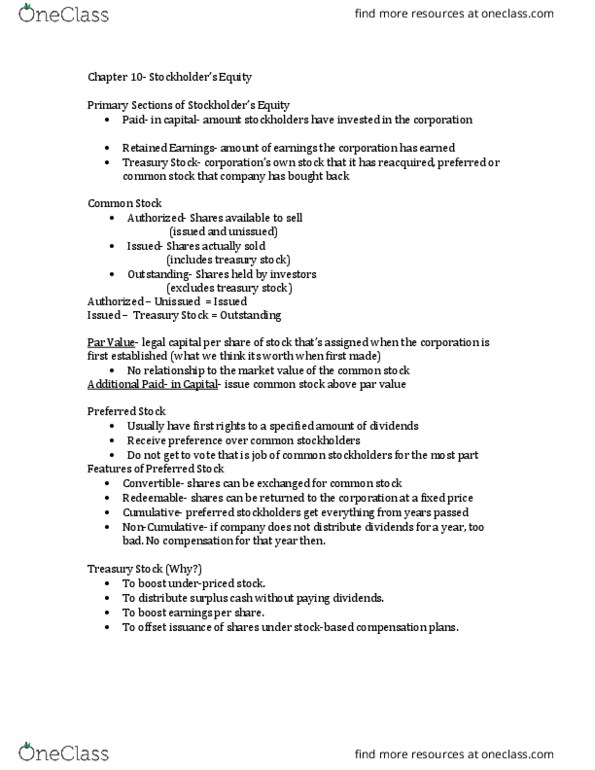

Chapter 10 – Stockholder’s Equity

Components of Stockholder’s Equity

oTreasury Stock – our own stock bought back from the marketplace

Paid-In Capital

oReview

i.e. we sell a share for $10

oPAR value = Money ($) on certificate

PAR value is a legal concept

Represents capital to be kept in business as final liquidating amount

i.e. Sell $10 PAR Share for $12

Since the stock is worth $10, but the company sells it for more,

the difference between what the stock was sold and what the PAR

value is will be the “additional paid-in capital”

find more resources at oneclass.com

find more resources at oneclass.com

oTypes of Stock

“Bucket” example

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Acct 201 lecture 12 chapter 10. Components of stockholder"s equity: treasury stock our own stock bought back from the marketplace. Paid-in capital: review i. e. we sell a share for , par value = money ($) on certificate. Represents capital to be kept in business as final liquidating amount i. e. sell par share for . Since the stock is worth , but the company sells it for more, the difference between what the stock was sold and what the par value is will be the additional paid-in capital : types of stock. Example question for the bucket example: the corporate charter of. Gigantic corporation allows the issuance of a maximum of 2,500 shares of par common stock. It later acquired 20 of these shares as treasure stock. Authorized is 2,500 as the company allowed that many to be available. Issued is 1,200 because that is how many had been currently sold.