01:220:102 Lecture Notes - Lecture 14: Perfect Competition, Marginal Revenue, Marginal Cost

19 Oct 2017

School

Department

Course

Professor

57

01:220:102 Full Course Notes

Verified Note

57 documents

Document Summary

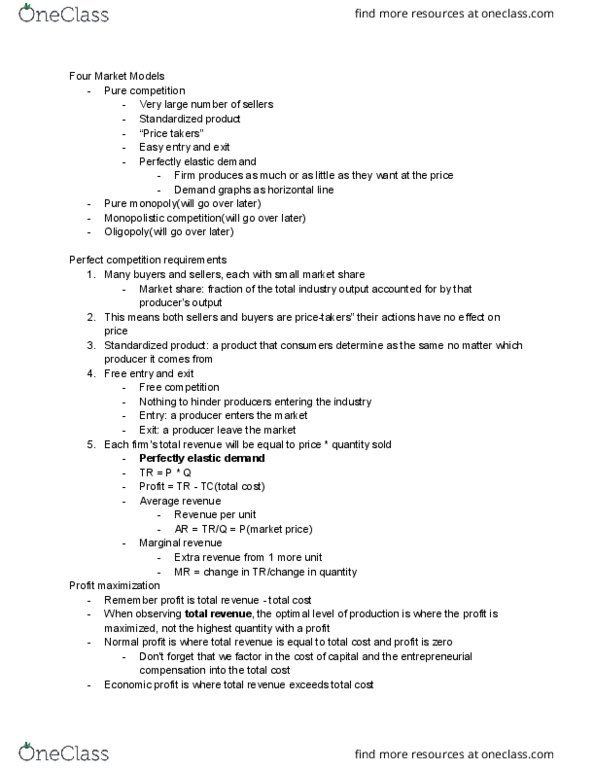

Price-taking producers: a producer whose actions have no effect on the market price of the good or service it sells. Price-taking consumer: a consumer whose actions have no effect on the market price of the good or service he or she buys. Perfectly competitive market: a market in which all market participants are price-takers. Perfectly competitive industry: an industry in which producers are price-takers. For an industry to be perfectly competitive, it must contain many producers, none of whom have a large market share. Market share: the fraction of the total industry output accounted for by that producer"s output. An industry can be perfectly competitive only if consumers regard the products of all producers as equivalent. An industry can be perfectly competitive only if it is easy for new firms to enter the industry or for firms that are currently in the industry to leave.