BFN 110 Lecture Notes - Lecture 15: Risk-Free Interest Rate, Risk Premium, Efficient-Market Hypothesis

20 views2 pages

6 Jan 2021

School

Department

Course

Professor

Document Summary

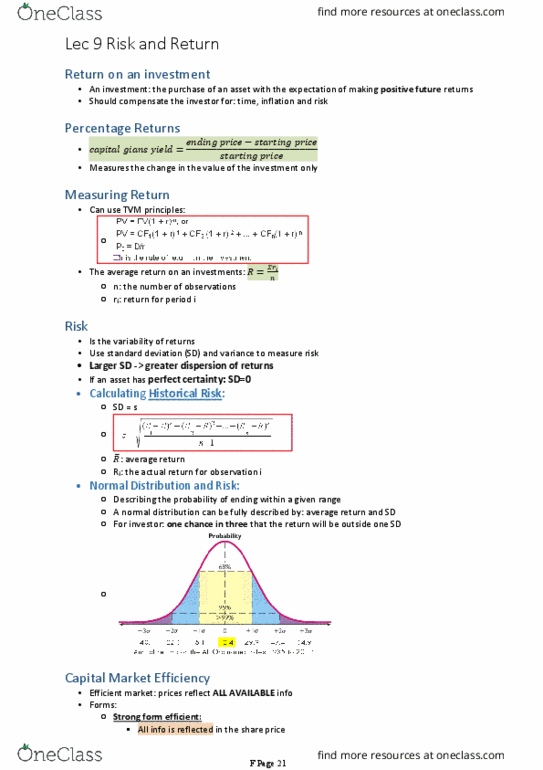

Calculate variance and standard deviation for an asset. Where r line is the average return. And ri is the actual return for observation i. If historical returns from an asset are 60%, -25% and 50% and avg return is 28. 33% S = square root [ (60-28. 33)2 + (-25-28. 33)2 + (50-28. 33)2. Prices of securities change due to new info arriving. If it"s very fast, then the market is said to be efficient. In an inefficient market, prices reflect all available info. All info is reflected in the share price. Investors cannot use public info to outperform the market. All public info reflected in share price. Trend or technical analysis cannot be used to find undervalued or. Assigning probabilities to different outcomes allows a measure of the return that can be expected in the long run. = sum of probability of return x return. An investor believes that the returns for an investment depends on the state of the economy.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers