ECON 1202 Lecture 7: Tariffs and Smith

ECON 1202 verified notes

7/29View all

Document Summary

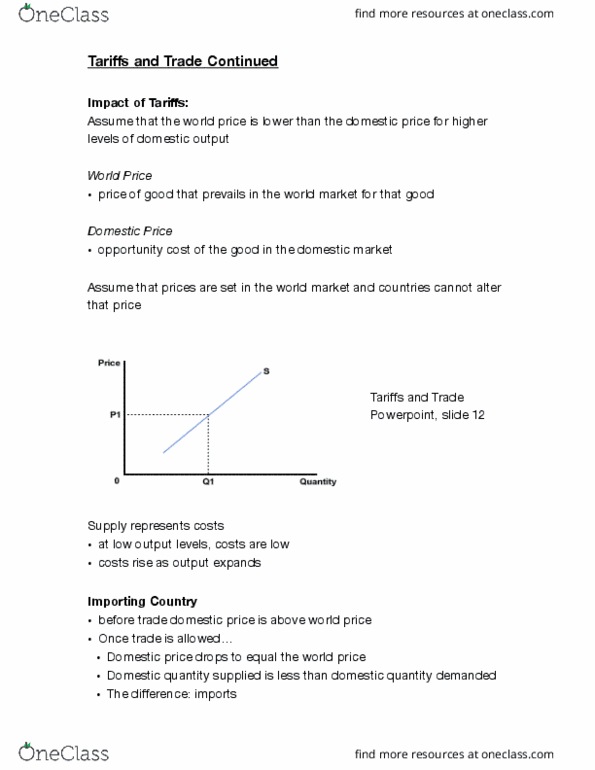

Assume that the world price is lower than the domestic price for higher levels of domestic output. World price: price of good that prevails in the world market for that good. Domestic price: opportunity cost of the good in the domestic market. Assume that prices are set in the world market and countries cannot alter that price. Supply represents costs: at low output levels, costs are low, costs rise as output expands. Importing country: before trade domestic price is above world price, once trade is allowed , domestic price drops to equal the world price, domestic quantity supplied is less than domestic quantity demanded, the di erence: imports. American consumers can buys as much steel as they want at world price: world price is lower than domestic price of steel, we in u. s. can consume as much as we want at that price.