BA 3301 Lecture Notes - Lecture 14: Cash Flow Statement, Financial Statement, Credit Risk

Document Summary

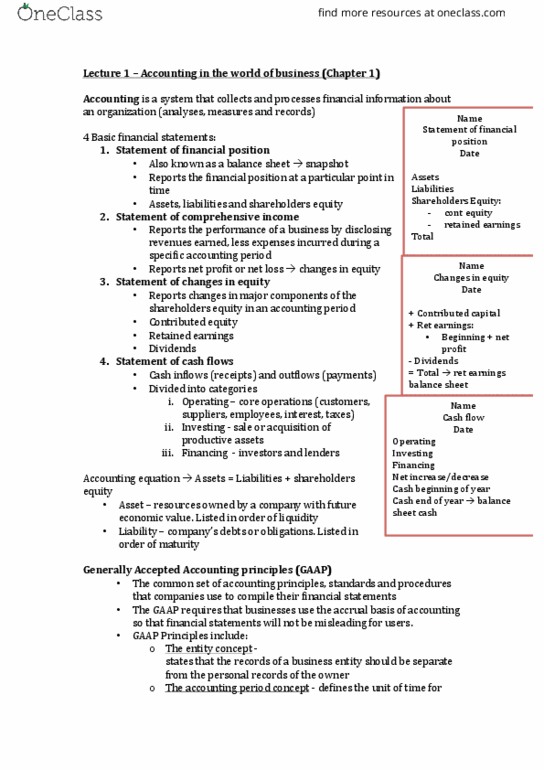

Accounting is the information system that measures business activity, processes data into. General purpose financial reports (income statement, balance sheet, cash flow statement) and ultimately communicates the results to decision makers. Financial accounting: provides information for external stakeholders (banks, ato, suppliers, shareholders) to allow users to make economic decisions about the entity. Investors/shareholders use this to measure profitability. (cid:380) (cid:380) banks use this to assess credit risk (ability to make loan repayments). Managerial accounting: provides information for internal stakeholders (management, Cfo, ceo) to manage a business and how to best run its operations. This allows management to: (cid:380) set future goals. (cid:380) monitor and control progress towards achieving goals. (cid:380) evaluate the degree to which previous goals were achieved. (cid:380) take corrective action when needed. The conceptual framework (cf) provides all the information required concerning basic accounting terms and concepts. Corporations law: qualitative characteristics, definition of elements of financial statements (cid:380) assets (cid:380) liabilities (cid:380) owner"s equity.