BUS 202 Lecture Notes - Lecture 3: Bizarre Inc, No Entry, Campbell Soup Company

Document Summary

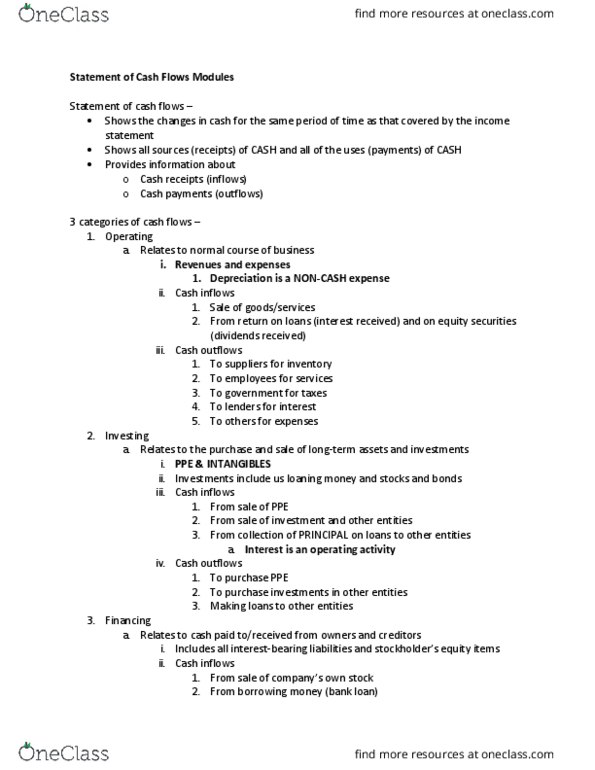

Describes inflows (sources) and outflows (applications or uses) Cash flows of the company used to predict cash flows to investors and creditors. How the balance sheet changed from the beginning of the year to the end of the year. Cash received (paid) due to activities reported in earnings under the accrual basis in the comprehensive income statement. Cash paid to acquire long-term assets and cash received upon their disposal. Raising and re-paying capital received from investors and creditors. Significant financing activities and investing activities specifically reported. Measures and reports results of operations in the comprehensive income statement in terms of earnings/profits. Receivables, payables, prepaid expenses, inventories, unearned revenues, deferrals. Overview of cash flow patterns in a typical business. Raises m in capital from investors (m) and creditors (m) Allocates m capital to long-term assets: pp&e (m) and intangibles (m) Cash paid for income taxes (12. 0m) (10. 0m) (0. 5m) (2. 7m) Income taxes (12. 0m) (10. 0m) (0. 6m) (0. 2m) (0. 5m) (2. 7m)